UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 25, 2010

|

Commission file number 1–6770

|

MUELLER INDUSTRIES, INC.

(Exact name of registrant as specified in its charter)

|

Delaware

|

25-0790410

|

|

(State or other jurisdiction

|

(I.R.S. Employer

|

|

of incorporation or organization)

|

Identification No.)

|

|

8285 Tournament Drive, Suite 150

|

|

|

Memphis, Tennessee

|

38125

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code: (901) 753-3200

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Name of each exchange on which registered

|

| |

|

|

Common Stock, $0.01 Par Value

|

New York Stock Exchange

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes S No £

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes £ No S

Indicate by a check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes S No £

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files).Yes S No £

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. S

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer S

|

Accelerated filer £

|

|

Non-accelerated filer £

|

Smaller reporting company £

|

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes £ No S

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the Registrant’s most recently completed second fiscal quarter was $908,404,764.

The number of shares of the Registrant’s common stock outstanding as of February 18, 2011 was 37,855,071 excluding 2,236,431 treasury shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the following document are incorporated by reference into this Report: Registrant’s Definitive Proxy Statement for the 2011 Annual Meeting of Stockholders, scheduled to be mailed on or about March 23, 2011 (Part III).

MUELLER INDUSTRIES, INC.

_____________________

As used in this report, the terms “Company,” “Mueller,” and “Registrant” mean Mueller Industries, Inc. and its consolidated subsidiaries taken as a whole, unless the context indicates otherwise.

____________________

| |

|

|

Page

|

|

Part I

|

|

|

| |

Item 1.

|

|

4

|

| |

Item 1A.

|

|

10

|

| |

Item 1B.

|

|

13

|

| |

Item 2.

|

|

14

|

| |

Item 3.

|

|

16

|

| |

|

|

|

|

Part II

|

|

|

| |

Item 5.

|

|

20

|

| |

Item 6.

|

|

22

|

| |

Item 7.

|

|

23

|

| |

Item 7A.

|

|

23

|

| |

Item 8.

|

|

23

|

| |

Item 9.

|

|

23

|

| |

Item 9A.

|

|

23

|

| |

Item 9B.

|

|

26

|

| |

|

|

|

|

Part III

|

|

|

| |

Item 10.

|

|

26

|

| |

Item 11.

|

|

26

|

| |

Item 12.

|

|

27

|

| |

Item 13.

|

|

28

|

| |

Item 14.

|

|

28

|

| |

|

|

|

|

Part IV

|

|

|

| |

Item 15.

|

|

28

|

| |

|

|

|

|

|

|

31

|

| |

|

|

|

|

|

F-1

|

PART I

Introduction

The Company is a leading manufacturer of copper, brass, plastic, and aluminum products. The range of these products is broad: copper tube and fittings; brass and copper alloy rod, bar, and shapes; aluminum and brass forgings; aluminum and copper impact extrusions; plastic pipe, fittings and valves; refrigeration valves and fittings; fabricated tubular products; and steel nipples. The Company also resells imported brass and plastic plumbing valves, malleable iron fittings, faucets and plumbing specialty products. Mueller's operations are located throughout the United States and in Canada, Mexico, Great Britain, and China.

The Company's businesses are aggregated into two reportable segments: the Plumbing & Refrigeration segment and the Original Equipment Manufacturers (OEM) segment. For disclosure purposes, as permitted under Accounting Standards Codification (ASC) 280, Segment Reporting, certain operating segments are aggregated into reportable segments. The Plumbing & Refrigeration segment is composed of the Standard Products Division (SPD), European Operations, and Mexican Operations. The OEM segment is composed of the Industrial Products Division (IPD), Engineered Products Division (EPD), and Jiangsu Mueller–Xingrong Copper Industries Limited (Mueller-Xingrong), the Company’s Chinese joint venture. Certain administrative expenses and expenses related primarily to retiree benefits at inactive operations are combined into the Corporate and Eliminations classification. These reportable segments are described in more detail below.

SPD manufactures and sells copper tube, copper and plastic fittings, plastic pipe, and valves in North America and sources products for import distribution in North America. European Operations manufacture copper tube in Europe, which is sold in Europe and the Middle East; activities also include import distribution in the U.K. and Ireland. Mexican Operations consist of pipe nipple manufacturing and import distribution businesses including product lines of malleable iron fittings and other plumbing specialties. The Plumbing & Refrigeration segment sells products to wholesalers in the HVAC (heating, ventilation, and air-conditioning), plumbing, and refrigeration markets, to distributors to the manufactured housing and recreational vehicle industries, and to building material retailers.

The OEM segment manufactures and sells brass and copper alloy rod, bar, and shapes; aluminum and brass forgings; aluminum and copper impact extrusions; refrigeration valves and fittings; fabricated tubular products; and gas valves and assemblies. Mueller-Xingrong manufactures engineered copper tube primarily for air-conditioning applications; these products are sold primarily to OEMs located in China. The OEM segment sells its products primarily to original equipment manufacturers, many of which are in the HVAC, plumbing, and refrigeration markets.

Information concerning segments and geographic information appears under “Note 15 - Industry Segments” in the Notes to Consolidated Financial Statements for the year ended December 25, 2010 in Item 8 of this Report, which is incorporated herein by reference.

The majority of the Company’s manufacturing facilities operated at significantly below capacity during 2010 and 2009 due to the reduced demand for the Company’s products arising from the general economic conditions in the U.S. and foreign markets that the Company serves. The U.S. housing and residential construction market has been adversely affected in the recent economic downturn. Per the U.S. Census Bureau, new housing starts in the U.S. were 588 thousand in 2010, which was a six percent increase compared with 554 thousand in 2009 and much lower than the historical amounts of 906 thousand in 2008 and 1.4 million in 2007. The December 2010 seasonally adjusted annual rate of new housing starts was 529 thousand, which is a decrease of eight percent compared with the December 2009 rate of 576 thousand. Housing construction activity and new home sales slowed significantly following the expiration of homebuyer tax incentives in April 2010. This is reflected in the year over year increase in housing starts and the year over year decrease in the December seasonally adjusted annual rates. Mortgage rates have remained at low levels during 2010 and 2009, as the average 30-year fixed mortgage rate was 4.71 percent in December 2010 and 4.93 percent in December 2009. Commercial construction has also declined significantly in the past two years. According to the U.S. Census Bureau, the private nonresidential value of construction put in place was $265.9 billion in 2010, $346.7 billion in 2009, and $408.6 billion in 2008. Business conditions in the U.S. automotive industry have also been exceptionally difficult in the economic downturn, which affected the demand for various products in the Company’s OEM segment; however, some improvements have recently occurred. All of these conditions have significantly affected the demand for virtually all of the Company’s core products.

The Company is a Delaware corporation incorporated on October 3, 1990.

Plumbing & Refrigeration Segment

Mueller’s Plumbing & Refrigeration segment includes SPD, which manufactures a broad line of copper tube, in sizes ranging from 1/8 inch to 8 inch diameter, which are sold in various straight lengths and coils. Mueller is a market leader in the air-conditioning and refrigeration service tube markets. Additionally, Mueller supplies a variety of water tube in straight lengths and coils used for plumbing applications in virtually every type of construction project. SPD also manufactures copper and plastic fittings and related components for the plumbing and heating industry that are used in water distribution systems, heating systems, air-conditioning, and refrigeration applications, and drainage, waste, and vent systems. A major portion of SPD’s products are ultimately used in the domestic residential and commercial construction markets.

The Plumbing & Refrigeration segment also fabricates steel pipe nipples and resells imported brass and plastic plumbing valves, malleable iron fittings, faucets, and plumbing specialty products to plumbing wholesalers, distributors to the manufactured housing and recreational vehicle industries and building materials retailers.

On August 6, 2010 the Company expanded its existing line sets business by purchasing certain assets from Linesets, Inc., a manufacturer of assembled line sets with operations in Phoenix, Arizona and Atlanta, Georgia. Net sales for the acquired operations were approximately $9.2 million in 2009.

The Plumbing & Refrigeration segment markets primarily through its own sales and distribution organization, which maintains sales offices and distribution centers throughout the United States and in Canada, Mexico, and Europe. Additionally, products are sold and marketed through a network of agents, which, when combined with the Company’s sales organization, provide the Company broad geographic market representation.

These businesses are highly competitive. The principal methods of competition for Mueller’s products are customer service, availability, and price. The total amount of order backlog for the Plumbing & Refrigeration segment as of December 25, 2010 was not significant.

The Company competes with various companies, depending on the product line. In the U.S. copper tubing business, the domestic competition includes Cerro Flow Products, Inc., Cambridge-Lee Industries LLC (a subsidiary of Industrias Unidas S.A. de C.V.), Wolverine Tube, Inc., KobeWieland Copper Products LLC, and Howell Metal Company (a subsidiary of Commercial Metals Company), as well as many actual and potential foreign competitors. In the European copper tubing business, Mueller competes with several European-based manufacturers of copper tubing as well as other foreign-based manufacturers. In the copper fittings market, competitors include Elkhart Products Company (a subsidiary of Aalberts Industries N.V.) and NIBCO, Inc., as well as several foreign manufacturers. Additionally, the Company’s copper tube and fittings businesses compete with a large number of manufacturers of substitute products made from other metals and plastic. The plastic fittings competitors include NIBCO, Inc., Charlotte Pipe & Foundry, and other companies. Management believes that no single competitor offers such a wide-ranging product line as Mueller and that this is a competitive advantage in some markets.

OEM Segment

Mueller’s OEM segment includes IPD, which manufactures brass rod, nonferrous forgings, and impact extrusions that are sold primarily to OEMs in the plumbing, refrigeration, fluid power, and automotive industries, as well as to other manufacturers and distributors. The Company extrudes brass, bronze, and copper alloy rod in sizes ranging from 3/8 inches to 4 inches in diameter. These alloys are used in applications that require a high degree of machinability, wear and corrosion resistance, as well as electrical conductivity. IPD also manufactures brass and aluminum forgings, which are used in a wide variety of products, including automotive components, brass fittings, industrial machinery, valve bodies, gear blanks, and computer hardware. IPD also serves the automotive, military ordnance, aerospace, and general manufacturing industries with cold-formed aluminum and copper impact extrusions. Typical applications for impacts are high strength ordnance, high-conductivity electrical components, builders’ hardware, hydraulic systems, automotive parts, and other uses where toughness must be combined with varying complexities of design and finish. The OEM segment also includes EPD, which manufactures and fabricates valves and custom OEM products for refrigeration and air-conditioning, gas appliance, and barbecue grill applications. Additionally EPD manufactures shaped and formed tube, produced to tight tolerances, for baseboard heating, appliances, and medical instruments. The total amount of order backlog for the OEM segment as of December 25, 2010 was not significant.

On December 28, 2010, the Company purchased certain assets from Tube Forming, L.P. (TFI). TFI has operations in Carrollton, Texas, and Guadalupe, Mexico, where it produces precision copper return bends and crossovers, and custom-made tube components and brazed assemblies, including manifolds and headers. TFI's estimated net sales for 2010 were approximately $35 million.

On February 27, 2007, the Company acquired 100 percent of the outstanding stock of Extruded Metals, Inc. (Extruded). Extruded, located in Belding, Michigan, manufactures brass rod products, and during 2006 had annual net sales of approximately $360 million. The acquisition of Extruded complements the Company’s existing brass rod product line.

In December 2005, two subsidiaries of the Company received a business license from a Chinese industry and commerce authority, establishing a joint venture with Jiangsu Xingrong Hi-Tech Co., Ltd. and Jiangsu Baiyang Industries Ltd. The joint venture, in which the Company holds a 50.5 percent interest, produces inner groove and smooth tube in level-wound coils, pancake coils, and straight lengths, primarily to serve the Chinese domestic OEM air-conditioning market as well as other copper products. The joint venture, which is located in Jintan City, Jiangsu Province, China, is named Jiangsu Mueller-Xingrong Copper Industries Limited (Mueller–Xingrong).

IPD and EPD primarily sell directly to OEM customers. Competitors, primarily in the brass rod market, include Chase Brass and Copper Company, a subsidiary of Global Brass and Copper, Inc., and others both domestic and foreign. Outside of North America, IPD and EPD sell products through various channels.

Labor Relations

At December 25, 2010, the Company employed approximately 3,600 employees, of which approximately 1,900 were represented by various unions. Those union contracts will expire as follows:

|

Location

|

Expiration Date

|

|

Port Huron, Michigan (Local 218 I.A.M.)

|

May 1, 2013

|

|

Port Huron, Michigan (Local 44 U.A.W.)

|

July 20, 2013

|

|

Belding, Michigan

|

August 15, 2012

|

|

Wynne, Arkansas

|

June 28, 2015

|

|

Fulton, Mississippi

|

August 1, 2012

|

|

North Wales, Pennsylvania

|

August 3, 2012

|

|

Waynesboro, Tennessee

|

November 9, 2012

|

The union agreements at the Company's U.K. and Mexico operations are renewed annually. The Company expects to renew the U.K. and Mexico contracts without material disruption of its operations.

Raw Material and Energy Availability

The major portion of Mueller’s base metal requirements (primarily copper) is normally obtained through short-term supply contracts with competitive pricing provisions (for cathode) and the open market (for scrap). Other raw materials used in the production of brass, including brass scrap, zinc, tin, and lead, are obtained from zinc and lead producers, open-market dealers, and customers with brass process scrap. Raw materials used in the fabrication of aluminum and plastic products are purchased in the open market from major producers.

Adequate supplies of raw material have historically been available to the Company from primary producers, metal brokers, and scrap dealers. Sufficient energy in the form of natural gas, fuel oils, and electricity is available to operate the Company’s production facilities. While temporary shortages of raw material and fuels may occur occasionally, to date they have not materially hampered the Company’s operations.

During recent years, an increasing demand for copper and copper alloy primarily from China had an effect on the global distribution of such commodities. The increased demand for copper (cathode and scrap) and copper alloy products from the export market, from time-to-time may cause a tightening in the domestic raw materials market. Mueller’s copper tube facilities can accommodate both refined copper and copper scrap as the primary feedstock. The Company has commitments from refined copper producers for a portion of its metal requirements for 2011. Adequate quantities of copper are currently available. While the Company will continue to react to market developments, resulting pricing volatility or supply disruptions, if any, could nonetheless adversely affect the Company.

Environmental Proceedings

Compliance with environmental laws and regulations is a matter of high priority for the Company. Mueller’s provision for environmental matters related to all properties was $5.4 million for 2010 and $1.1 million for 2009. The reserve for environmental matters was $23.9 million at December 25, 2010 and $23.3 million at December 26, 2009. Environmental costs related to non-operating properties are classified as a component of other (expense) income, net and costs related to operating properties are included in cost of goods sold. The Company does not anticipate that it will need to make material expenditures for compliance activities related to existing environmental matters during the remainder of the 2011 fiscal year, or for the next two fiscal years.

Non-operating Properties

Southeast Kansas Sites

By letter dated October 10, 2006, the Kansas Department of Health and Environment (KDHE) advised the Company that environmental contamination has been identified at a former smelter site in southeast Kansas. KDHE asserts that the Company is a corporate successor to an entity that is alleged to have owned and operated the smelter from 1915 to 1918. The Company has since been advised of a possible connection between that same entity and two other former smelter sites in Kansas. KDHE has requested that the Company and other potentially responsible parties (PRPs) negotiate a consent order with KDHE to address contamination at these sites. The Company has participated in preliminary discussions with KDHE and the other PRPs. The Company believes it is not liable for the contamination but as an alternative to litigation, the Company has entered into settlement negotiations with one of the other PRPs. The negotiations are ongoing. In 2008, the Company established a reserve of $9.5 million for this matter. Due to the ongoing nature of negotiations, the timing of potential payment has not yet been determined. The Company has also agreed to share the costs of a preliminary site assessment at one of the former smelter sites with two other PRPs.

Eureka Mills Site

On December 2, 2010, the United States District Court for Utah entered a consent decree between the Company, the United States and the State of Utah. The decree resolves the claims asserted by the U.S. and the State of Utah related to Eureka Mills Superfund Site located in Juab County, Utah. The Company’s connection to the Eureka Mills Site is through land within the site that was owned by Sharon Steel Corporation (Sharon), its predecessor, and a 1979 transaction with UV Industries (UV) in which Sharon allegedly assumed certain of UV’s liabilities. The Company has provided $2.5 million to settle its claims, of which $250 thousand was paid to the State of Utah in December 2010 and the remainder was paid to the U.S. in February 2011.

Shasta Area Mine Sites

Mining Remedial Recovery Company (MRRC), a wholly owned subsidiary, owns certain inactive mines in Shasta County, California. MRRC has continued a program, begun in the late 1980’s, of sealing mine portals with concrete plugs in mine adits which were discharging water. The sealing program has achieved significant reductions in the metal load in discharges from these adits; however, additional reductions are required pursuant to an order issued by the California Regional Water Quality Control Board (QCB). In response to a 1996 Order issued by the QCB, MRRC completed a feasibility study in 1997 describing measures designed to mitigate the effects of acid rock drainage. In December 1998, the QCB modified the 1996 order extending MRRC’s time to comply with water quality standards. In September 2002, the QCB adopted a new order requiring MRRC to adopt Best Management Practices (BMP) to control discharges of acid mine drainage. That order extended the time to comply with water quality standards until September 2007. During that time, implementation of BMP further reduced impacts of acid rock drainage; however full compliance has not been achieved. The QCB is presently renewing MRRC’s discharge permit and will concurrently issue a new order. It is expected that the new permit will include an order requiring continued implementation of BMP through 2015 to address residual discharges of acid rock drainage. At this site, MRRC spent approximately $0.7 million in 2010, $0.5 million in 2009, and $0.5 million in 2008, and estimates that it will spend between approximately $8.6 million and $11.3 million over the next 20 years.

Lead Refinery Site

U.S.S. Lead Refinery, Inc. (Lead Refinery), a non-operating wholly owned subsidiary of MRRC, has conducted corrective action and interim remedial activities and studies (collectively, Site Activities) at Lead Refinery’s East Chicago, Indiana site pursuant to the Resource Conservation and Recovery Act. Site Activities, which began in December 1996, have been substantially concluded. Lead Refinery is required to perform monitoring and maintenance activities with respect to Site Activities pursuant to a post-closure permit issued by the Indiana Department of Environmental Management (IDEM) effective as of January 22, 2008. Lead Refinery spent approximately $0.1 million annually in 2010, 2009, and 2008 with respect to this site. Approximate costs to comply with the post-closure permit, including associated general and administrative costs, are between $2.1 million and $3.2 million over the next 20 years.

On April 9, 2009, pursuant to the Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA), the U.S. Environmental Protection Agency (EPA) added the Lead Refinery site to the National Priorities List (NPL). The NPL is a list of priority sites where the EPA has determined that there has been a release or threatened release of contaminants that warrant investigation and, if appropriate, remedial action. The NPL does not assign liability to any party, owner or operator or to the owner of a property placed on the NPL. The placement of a site on the NPL does not necessarily mean that remedial action must be taken. On July 17, 2009, Lead Refinery received a written notice from the EPA that the agency is of the view that Lead Refinery may be a PRP under CERCLA in connection with the release or threat of release of hazardous substances including lead into a residential area adjacent to the site. PRPs under CERCLA include current and former owners and operators of a site, persons who arranged for disposal or treatment of hazardous substances at a site, or persons who accepted hazardous substances for transport to a site. The Company is unable to determine the likelihood of a material adverse outcome or the amount or range of a potential loss with respect to placement of this site on the NPL or in connection with the notice of potential liability concerning the residential area. Lead Refinery lacks the financial resources needed to undertake any investigations or remedial action that may be required by the EPA pursuant to CERCLA.

Operating Properties

Mueller Copper Tube Products, Inc.

In 1999, Mueller Copper Tube Products, Inc. (MCTP), a wholly owned subsidiary, commenced a cleanup and remediation of soil and groundwater at its Wynne, Arkansas plant. MCTP is currently removing trichloroethylene, a cleaning solvent formerly used by MCTP, from the soil and groundwater. On August 30, 2000, MCTP received approval of its Final Comprehensive Investigation Report and Storm Water Drainage Investigation Report addressing the treatment of soils and groundwater from the Arkansas Department of Environmental Quality (ADEQ). The Company established a reserve for this project in connection with the acquisition of MCTP in 1998. Effective November 17, 2008, MCTP entered into a Settlement Agreement and Administrative Order by Consent to submit a Supplemental Investigation Work Plan (SIWP) and subsequent Final Remediation Work Plan for the site. By letter dated January 20, 2010, ADEQ approved the SIWP as submitted, with changes acceptable to the Company. Costs to implement the work plans, including associated general and administrative costs, are approximately $0.6 million over the next 10 years.

Belding, Michigan Lead Matters

In 2009 and 2010, in response to requests from the Michigan Department of Natural Resources and Environment (MDNRE), Extruded Metals, Inc. (Extruded), a wholly owned subsidiary, conducted stack emissions testing of the stationary sources at its Belding, Michigan facility (the Belding Facility). The results of tests on the West Chip Dryer showed non-compliance with certain emission limitation in the facility’s air use permit for that process, including the limitation for lead. Modifications were made to the emissions control equipment on the West Chip Dryer, and subsequent testing demonstrated all stationary sources at the Belding Facility to be in compliance with the requirements of their air use permits.

In December 2009 and August 2010, the MDNRE issued a notice of violation and an enforcement notice with respect to the prior permit violations with respect to the West Chip Dryer. Extruded will be required to enter into an administrative consent order (ACO) with the MDNRE to resolve the allegations contained in the notices. The MDNRE has advised that it intends to impose a civil fine as part of the resolution of those allegations. The MDNRE has not advised Extruded as to the amount of the fine it intends to impose.

Beginning in January 2009, and in response to the EPA’s 2008 order of magnitude reduction of the national ambient air quality standard (NAAQS) for lead, the MDNRE began monitoring ambient air lead levels in areas of the State of Michigan where stationary sources of lead emissions were known to be present. Ambient air monitoring downwind of the Belding Facility demonstrated periodic exceedances of the new NAAQS for lead. The MDNRE requested that Extruded submit an application for a new air use permit for the Belding Facility that will ensure compliance with that new federal standard. The application was submitted on January 21, 2011. The application proposes raising the stack height on the facility’s two chip dryers. It is unknown whether the MDNRE will approve the application and what the ultimate cost of complying with the new NAAQS may be.

In October 2010, the MDNRE conducted testing of lead levels in soils on properties upwind and downwind of the Belding Facility. Results of that testing showed exceedances of the Michigan generic residential direct contact cleanup criteria for lead on a number of the downwind properties. Extruded has agreed with the MDNRE to investigate the extent of this condition and to perform remediation to the extent required by environmental laws. Extruded has solicited proposals from a number of environmental consulting firms to assist it in these efforts. A firm has been selected, and with their assistance, a conceptual interim response plan was submitted to the MDNRE. The Company is awaiting a response to this plan. The Company established a reserve for $0.4 million in 2010 for this matter, and is pursuing potential remedies from the previous owner.

In November 2010, Extruded received a request for information under Section 114(a) of the Clean Air Act from the EPA. The focus of the EPA’s information request was the Belding Facility’s compliance with the National Emissions Standards for Hazardous Air Pollutants for Secondary Nonferrous Metals Processing Area Sources, 40 C.F.R. § 63.114679 (Subpart TTTTTT). Extruded responded to the information request and advised the EPA that it was not subject to regulation under Subpart TTTTTT.

Other

In connection with acquisitions, the Company established environmental reserves to fund the cost of remediation at sites currently or formerly owned by various acquired entities. The Company, through its acquired subsidiaries, is engaged in ongoing remediation and site characterization studies.

Health and Safety Matters

On January 25, 2010, the Company received Citations and a Notification of Penalties from the Occupational Safety and Health Administration (OSHA) proposing civil penalties totaling approximately $0.7 million for various health and safety violations following inspections in 2009 of certain plants operated by subsidiaries in Fulton, Mississippi. The Company has executed a final agreement with OSHA and the penalties have been reduced to approximately $0.4 million. The resolution of these matters did not have a material adverse effect on the Company’s financial condition, results of operations or cash flows.

Other Business Factors

The Registrant’s business is not materially dependent on patents, trademarks, licenses, franchises, or concessions held. In addition, expenditures for company-sponsored research and development activities were not material during 2010, 2009, or 2008. No material portion of the Registrant’s business involves governmental contracts. Seasonality of the Company’s sales is not significant.

SEC Filings

We make available through our internet website our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission (SEC). To retrieve any of this information, you may access our internet home page at www.muellerindustries.com, select Mueller Financials, and then select SEC Filings.

Reports filed with the SEC may also be viewed or obtained at the SEC Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Information on the operation of the SEC Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC maintains a website that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC; the website address is www.sec.gov.

The Company is exposed to risk as it operates its businesses. To provide a framework to understand the operating environment of the Company, we are providing a brief explanation of the more significant risks associated with our businesses. Although we have tried to identify and discuss key risk factors, others could emerge in the future. These risk factors should be considered carefully when evaluating the Company and its businesses.

Increases in costs and the availability of energy and raw materials used in our products could impact our cost of goods sold and our distribution expenses, which could have a material adverse impact on our operating margins.

Both the costs of raw materials used in our manufactured products (copper, brass, zinc, aluminum, and PVC and ABS resins) and energy costs (electricity, natural gas and fuel) have been volatile during the last several years, which has resulted in changes in production and distribution costs. For example, recent and pending climate change regulation and initiatives on the state, regional, federal, and international levels that have focused on reducing greenhouse gas (GHG) emissions from the energy and utility sectors may affect energy availability and costs in the near future. While we typically attempt to pass costs through to our customers or to modify or adapt our activities to mitigate the impact of increases, we may not be able to do so successfully. Failure to fully pass increases to our customers or to modify or adapt our activities to mitigate the impact could have a material adverse impact on our operating margins. Additionally, if we are for any reason unable to obtain raw materials or energy, our ability to manufacture our finished goods would be impacted which could have a material adverse impact on our operating margins.

The unplanned departure of key personnel could disrupt our business.

We depend on the continued efforts of our senior management. The unplanned loss of key personnel, or the inability to hire and retain qualified executives, could negatively impact our ability to manage our business.

Economic conditions in the housing and commercial construction industries as well as changes in interest rates could have a material adverse impact on our business, financial condition, and results of operations.

Our businesses are sensitive to changes in general economic conditions, including, in particular, conditions in the housing and commercial construction industries. Prices for our products are affected by overall supply and demand in the market for our products and for our competitors’ products. In particular, market prices of building products historically have been volatile and cyclical, and we may be unable to control the timing and amount of pricing changes for our products. Prolonged periods of weak demand or excess supply in any of our businesses could negatively affect our revenues and margins and could result in a material adverse impact on our business, financial condition, and results of operations.

The markets that we serve, including, in particular, the housing and commercial construction industries, are significantly affected by movements in interest rates and the availability of credit. Significantly higher interest rates could have a material adverse effect on our business, financial condition, and results of operations. Our businesses are also affected by a variety of other factors beyond our control, including, but not limited to, employment levels, foreign currency exchange rates, unforeseen inflationary pressures, and consumer confidence. Since we operate in a variety of geographic areas, our businesses are subject to the economic conditions in each such area. General economic downturns or localized downturns in the regions where we have operations could have a material adverse effect on our business, financial condition, and results of operations.

The recent deterioration of the general economic environment, distress in the financial markets and general uncertainty about the economy is having a significant negative impact on businesses and consumers around the world. The well-publicized downturn in the construction markets, both residential and commercial, including construction lending, may result in protracted decreased demand for our products. In addition, the impact of the economy on the operations or liquidity of any party with which we conduct our business, including our suppliers and customers, may adversely impact our business. We are unsure of the duration and severity of this economic crisis. However, if the crisis persists or worsens and economic conditions remain weak over a long period, the likelihood of the crisis having a significant impact on our business increases.

Competitive conditions including the impact of imports and substitute products could have a material adverse effect on our margins and profitability.

The markets we serve are competitive across all product lines. Some consolidation of customers has occurred and may continue, which could shift buying power to customers. In some cases, customers have moved production to low-cost countries such as China, or sourced components from there, which has reduced demand in North America for some of the products we produce. These conditions could have a material adverse impact on our ability to maintain margins and profitability. The potential threat of imports and substitute products is based upon many factors including raw material prices, distribution costs, foreign exchange rates, and production costs. The end use of alternative import and/or substitute products could have a material adverse effect on our business, financial condition, and results of operations.

Our exposure to exchange rate fluctuations on cross border transactions and the translation of local currency results into U.S. dollars could have an adverse impact on our results of operations or financial position.

We conduct our business through subsidiaries in several different countries and export our products to many countries. Fluctuations in currency exchange rates could have a significant impact on the competitiveness of our products as well as the reported results of our operations, which are presented in U.S. dollars. A significant and growing portion of our products are manufactured in, or acquired from suppliers located in, lower cost regions. Cross border transactions, both with external parties and intercompany relationships, result in increased exposure to foreign exchange fluctuations. The strengthening of certain currencies such as the euro and U.S. dollar could expose our U.S. based businesses to competitive threats from lower cost producers in other countries such as China. Lastly, our sales are translated into U.S. dollars for reporting purposes. The strengthening of the U.S. dollar could result in unfavorable translation effects when the results of foreign operations are translated into U.S. dollars. Accordingly, significant changes in exchange rates, particularly the U.K. pound sterling, Mexican peso, and the Chinese renminbi, could have an adverse impact on our results of operations or financial position.

We are subject to claims, litigation, and regulatory proceedings that could have a material adverse effect on us.

We are, from time–to-time, involved in various claims, litigation matters, and regulatory proceedings. These matters may include, among other things, contract disputes, personal injury claims, environmental claims, OSHA inspections or proceedings, other tort claims, employment and tax matters and other litigation including class actions that arise in the ordinary course of our business. Although we intend to defend these matters vigorously, we cannot predict with certainty the outcome or effect of any claim or other litigation matter, and there can be no assurance as to the ultimate outcome of any litigation or regulatory proceeding. Litigation and regulatory proceedings may have a material adverse effect on us because of potential adverse outcomes, defense costs, the diversion of our management’s resources, availability of insurance coverage and other factors.

A strike, other work stoppage or business interruption, or our inability to renew collective bargaining agreements on favorable terms, could impact our cost structure and our ability to operate our facilities and produce our products, which could have an adverse effect on our results of operations.

As of December 25, 2010, approximately one-half of our 3,600 employees were covered by collective bargaining or similar agreements. If we are unable to negotiate acceptable new agreements with the unions representing our employees upon expiration of existing contracts, we could experience strikes or other work stoppages. Strikes or other work stoppages could cause a significant disruption of operations at our facilities, which could have an adverse impact on us. New or renewal agreements with unions representing our employees could call for higher wages or benefits paid to union members, which would increase our operating costs and could adversely affect our profitability. Higher costs and/or limitations on our ability to operate our facilities and produce our products resulting from increased labor costs, strikes or other work stoppages could have an adverse effect on our results of operations.

In addition, unexpected interruptions in our operations or those of our customers or suppliers due to such causes as weather-related events or acts of God, such as earthquakes, could have an adverse effect on our results of operations. For example, the EPA has recently found that global climate change would be expected to increase the severity and possibly the frequency of severe weather patterns such as hurricanes. Although the financial impact of such is not reasonably estimable at this time, should such occur, our operations in certain coastal and flood-prone areas or operations of our customers and suppliers could be adversely affected.

We are subject to environmental and health and safety laws and regulations and future compliance may have a material adverse effect on our results of operations or financial position.

The nature of our operations exposes us to the risk of liabilities and claims with respect to environmental matters and health and safety matters. While we have established accruals intended to cover the cost of environmental remediation at contaminated sites, the actual cost is difficult to determine and may exceed our estimated reserves. Further, changes to, or more rigorous enforcement or stringent interpretation of environmental or health and safety laws could require significant incremental costs to maintain compliance. Recent and pending climate change regulation and initiatives on the state, regional, federal, and international levels may require certain of our facilities to reduce GHG emissions. While not reasonably estimable at this time, this could require capital expenditures for environmental control facilities and/or the purchase of GHG emissions credits in the coming years. In addition, with respect to environmental matters, future claims may be asserted against us for, among other things, past acts or omissions at locations operated by predecessor entities, or alleging damage or injury or seeking other relief in connection with environmental matters associated with our operations. Future liabilities, claims and compliance costs may have a material adverse effect on us because of potential adverse outcomes, defense costs, the diversion of our management's resources, availability of insurance coverage and other factors.

None.

Information pertaining to the Registrant’s major operating facilities is included below. Except as noted, the Registrant owns all of its principal properties. The Registrant’s plants are in satisfactory condition and are suitable for the purpose for which they were designed and are now being used.

| |

|

|

|

|

|

|

|

Location

|

|

Approximate Property Size

|

|

|

Description

|

| |

|

|

|

|

|

|

|

Plumbing & Refrigeration Segment

|

|

|

|

|

| |

|

|

|

|

| |

Fulton, MS

|

|

418,000 sq. ft.

52.37 acres

|

|

|

Copper tube mill. Facility includes casting, extruding, and finishing equipment to produce copper tubing, including tube feedstock for the Company’s copper fittings plants and Precision Tube factory.

|

| |

|

|

|

|

|

|

| |

Fulton, MS

|

|

103,000 sq. ft.

11.9 acres

|

|

|

Casting facility. Facility includes casting equipment to produce copper billets used in the adjoining copper tube mill.

|

| |

|

|

|

|

|

|

| |

Wynne, AR

|

|

682,000 sq. ft.

39.2 acres

|

(1)

|

|

Copper tube mill and plastic fittings plant. Facility includes casting, extruding, and finishing equipment to produce copper tubing and copper tube line sets, and produces DWV fittings using injection molding equipment.

|

| |

|

|

|

|

|

|

| |

Fulton, MS

|

|

58,500 sq. ft.

15.53 acres

|

|

|

Packaging and bar coding facility for retail channel sales.

|

| |

|

|

|

|

|

|

| |

Fulton, MS

|

|

70,000 sq. ft.

7.68 acres

|

(2)

|

|

Copper fittings plant. High-volume facility that produces copper fittings using tube feedstock from the Company’s adjacent copper tube mill.

|

| |

|

|

|

|

|

|

| |

Covington, TN

|

|

159,500 sq. ft.

40.88 acres

|

|

|

Copper fittings plant. Facility produces copper fittings using tube feedstock from the Company’s copper tube mills.

|

| |

|

|

|

|

|

|

| |

Ontario, CA

|

|

211,000 sq. ft.

10 acres

|

(3)

|

|

Distribution center and plastics manufacturing plant. Produces DWV fittings using injection molding equipment and ABS plastic pipe using pipe extruders.

|

| |

|

|

|

|

|

|

| |

Fort Pierce, FL

|

|

69,875 sq. ft.

5.60 acres

|

|

|

Plastic fittings plant. Produces pressure fittings using injection molding equipment.

|

| |

|

|

|

|

|

|

| |

Monterrey, Mexico

|

|

120,000 sq. ft.

3.4 acres

|

(3)

|

|

Pipe nipples plant. Produces pipe nipples, cut pipe and merchant couplings.

|

| |

|

|

|

|

|

|

| |

Bilston, England, United Kingdom

|

|

402,500 sq. ft.

14.95 acres

|

|

|

Copper tube mill. Facility includes casting, extruding, and finishing equipment to produce copper tubing.

|

| |

|

|

|

|

|

|

| |

Phoenix, AZ

|

|

26,000 sq. ft.

|

(3)

|

|

Line sets plant. Produces standard and custom made line sets for HVAC markets.

|

| |

|

|

|

|

|

|

| |

Atlanta, GA

|

|

24,000 sq. ft.

|

(3)

|

|

Line sets plant. Produces standard and custom made line sets for HVAC markets.

|

| |

|

|

|

|

|

|

(continued)

ITEM 2. PROPERTIES

|

(continued)

|

|

|

|

|

|

| |

Location

|

|

Approximate Property Size

|

|

|

Description

|

| |

|

|

|

|

|

|

|

OEM Segment

|

|

|

|

|

| |

|

|

|

|

| |

Port Huron, MI

|

|

322,500 sq. ft.

71.5 acres

|

|

|

Brass rod mill. Facility includes casting, extruding, and finishing equipment to produce brass rods and bars, in various shapes and sizes.

|

| |

|

|

|

|

|

|

| |

Belding, MI

|

|

293,068 sq. ft.

17.64 acres

|

|

|

Brass rod mill. Facility includes casting, extruding, and finishing equipment to produce brass rods and bars, in various shapes and sizes.

|

| |

|

|

|

|

|

|

| |

Port Huron, MI

|

|

127,500 sq. ft.

|

|

|

Forgings plant. Produces brass and aluminum forgings.

|

| |

|

|

|

|

|

|

| |

Marysville, MI

|

|

81,500 sq. ft.

6.72 acres

|

|

|

Aluminum and copper impacts plant. Produces made-to-order parts using cold impact processes.

|

| |

|

|

|

|

|

|

| |

Hartsville, TN

|

|

78,000 sq. ft.

4.51 acres

|

|

|

Refrigeration products plant. Produces products used in refrigeration applications such as ball valves, line valves, and compressor valves.

|

| |

|

|

|

|

|

|

| |

Carthage, TN

|

|

67,520 sq. ft.

10.98 acres

|

|

|

Fabrication facility. Produces precision tubular components and assemblies.

|

| |

|

|

|

|

|

|

| |

Waynesboro, TN

|

|

57,000 sq. ft.

5.0 acres

|

(4)

|

|

Gas valve plant. Facility produces brass and aluminum valves and assemblies for the gas appliance industry.

|

| |

|

|

|

|

|

|

| |

North Wales, PA

|

|

174,000 sq. ft.

18.9 acres

|

|

|

Precision Tube factory. Facility fabricates copper tubing, copper alloy tubing, aluminum tubing, and fabricated tubular products.

|

| |

|

|

|

|

|

|

| |

Brighton, MI

|

|

65,000 sq. ft.

|

(3)

|

|

Machining operation. Facility machines component parts for supply to automotive industry.

|

| |

|

|

|

|

|

|

| |

Middletown, OH

|

|

55,000 sq. ft.

2.0 acres

|

|

|

Fabricating facility. Produces burner systems and manifolds for the gas appliance industry.

|

| |

|

|

|

|

|

|

| |

Jintan City, Jiangsu Province, China

|

|

322,580 sq. ft

33.0 acres

|

(5)

|

|

Copper tube mill. Facility includes casting, and finishing equipment to produce engineered copper tube primarily for OEMs.

|

| |

|

|

|

|

|

|

| |

Xinbei District, Changzhou, China

|

|

33,940 sq. ft

|

(3)

|

|

Refrigeration products plant. Produces products used in refrigeration applications such as ball valves, line valves, and compressor valves.

|

| |

|

|

|

|

|

|

| |

Carrollton, TX

|

|

166,000 sq. ft.

|

(3)

|

|

Fabrication facility. Produces tubular components, assemblies, and return bends for refrigeration and HVAC markets.

|

| |

|

|

|

|

|

|

In addition, the Company owns and/or leases other properties used as distribution centers and corporate offices.

|

(1)

|

Facility, or some portion thereof, is located on land leased from a local municipality, with an option to purchase at nominal cost.

|

|

(2)

|

Facility is leased under a long-term lease agreement, with an option to purchase at nominal cost.

|

|

(3)

|

Facility is leased under an operating lease.

|

|

(4)

|

Facility is leased from a local municipality for a nominal amount.

|

|

(5)

|

Facility is located on land that is under a long-term land use rights agreement.

|

General

The Company is involved in certain litigation as a result of claims that arose in the ordinary course of business. Additionally, the Company may realize the benefit of certain legal claims and litigation in the future; these gain contingencies are not recognized in the Consolidated Financial Statements.

Environmental Proceedings

Reference is made to “Environmental Matters” in Item 1 of this Report, which is incorporated herein by reference, for a description of environmental proceedings.

Carrier ACR Copper Tube Action

The Company has been named as a defendant in a pending litigation (the Carrier ACR Tube Action) brought by Carrier Corporation, Carrier S.A., and Carrier Italia S.p.A. (collectively, Carrier), direct purchasers of copper tube. The Carrier ACR Tube Action was filed in March 2006 in the United States District Court for the Western District of Tennessee. The Carrier ACR Tube Action alleges anticompetitive activities with respect to the sale of copper tubes used in, among other things, the manufacturing of air-conditioning and refrigeration units (ACR copper tubes). The Company and Mueller Europe, Limited (Mueller Europe) are named in the Carrier ACR Tube Action. The Carrier ACR Tube Action seeks monetary and other relief.

In July 2007, the Carrier ACR Tube Action was dismissed in its entirety for lack of subject matter jurisdiction as to all defendants. In August 2007, plaintiffs filed with the United States Court of Appeals for the Sixth Circuit a notice of appeal from the judgment and order dismissing the complaint in the Carrier ACR Tube Action. The Company and Mueller Europe filed notices of cross-appeal in August 2007.

In October 2007, Carrier filed with the United States Court of Appeals for the Sixth Circuit a motion to dismiss the cross-appeals, which the Court denied in December 2007. All appeals in the Carrier ACR Tube Action remain pending. Briefing on the appeals occurred in May 2009 and oral argument took place in October 2009.

Although the Company believes that the claims for relief in the Carrier ACR Tube Action are without merit, due to the procedural stage of the Carrier ACR Tube Action, the Company is unable to determine the likelihood of a material adverse outcome in the Carrier ACR Tube Action or the amount or range of a potential loss in the Carrier ACR Tube Action.

Canadian Dumping and Countervail Investigation

In June 2006, the Canada Border Services Agency (CBSA) initiated an investigation into the alleged dumping of certain copper pipe fittings from the United States and from South Korea, and the dumping and subsidizing of these same goods from China. The Company and certain affiliated companies were identified by the CBSA as exporters and importers of these goods.

On January 18, 2007, the CBSA issued a final determination in its investigation. The Company was found to have dumped subject goods during the CBSA’s investigation period. On February 19, 2007, the Canadian International Trade Tribunal (CITT) concluded that the dumping of the subject goods from the United States had caused injury to the Canadian industry.

As a result of these findings, exports of subject goods to Canada by the Company made on or after October 20, 2006 have been subject to antidumping measures. Under Canada’s system of prospective antidumping enforcement, the CBSA has issued normal values to the Company. Antidumping duties will be imposed on the Company only to the extent that the Company’s future exports of copper pipe fittings are made at net export prices which are below these normal values. If net export prices for subject goods exceed normal values, no antidumping duties will be payable. These measures will remain in place for five years, at which time an expiry review will be conducted by Canadian authorities to determine whether these measures should be maintained for another five years or allowed to expire.

On April 8, 2011, the CBSA will complete a review process pursuant to which revised normal values will be issued to exporters of subject goods, including the Company. Depending on the level of the newly revised normal values relative to the normal values and selling prices of the Company's competitors in Canada, the Company's sales of subject goods in Canada may increase or decrease relative to prior levels. In any event, given the small percentage of its products that are sold for export to Canada, the Company does not anticipate any material adverse effect on its financial condition, results of operations or cash flows as a result of the antidumping case in Canada.

The “sunset review” process, pursuant to which Canadian authorities will examine whether the dumping order should be revoked or maintained for another five years, will initiate in April 2011.

United States Department of Commerce Antidumping Review

On December 24, 2008, the United States Department of Commerce (DOC) initiated an antidumping administrative review of the antidumping duty order covering circular welded non-alloy steel pipe and tube from Mexico to determine the final antidumping duties owed on U.S. imports during the period November 1, 2007 through October 31, 2008 by certain subsidiaries of the Company. On April 19, 2010, DOC published the final results of this review and assigned Mueller Comercial de Mexico, S. de R.L. de C.V. (Mueller Comercial) an antidumping duty rate of 48.33 percent. The Company has appealed the final determination to the U.S. Court of International Trade. The Company anticipates that certain of its subsidiaries will incur antidumping duties on subject imports made during the period of review and as such established a reserve of approximately $4.2 million for this matter.

On December 23, 2009, the DOC initiated an antidumping administrative review of the antidumping duty order covering circular welded non-alloy steel pipe and tube from Mexico for the November 1, 2008 through October 31, 2009 period of review. The DOC selected Mueller Comercial as a respondent for this period of review. On December 15, 2010, the DOC issued preliminary results and assigned a margin of dumping of 4.81 percent to Mueller Comercial. Final results are expected no later than June 2011. At this time, the Company is unable to estimate the impact, if any, that this matter will have on its financial position, results of operations, or cash flows.

On December 28, 2010, the DOC initiated an antidumping administrative review of the antidumping duty order covering circular welded non-alloy steel pipe and tube from Mexico for the November 1, 2009 through October 31, 2010 period of review. The DOC has selected Mueller Comercial as a respondent for this period of review. At this time, the Company is unable to estimate the impact, if any, that this matter will have on its financial position, results of operations, or cash flows.

United States Department of Commerce and United States International Trade Commission Antidumping Investigations

On September 30, 2009, two subsidiaries of Mueller Industries, Inc., along with Cerro Flow Products, Inc. and KobeWieland Copper Products LLC (collectively, Petitioners), jointly filed antidumping petitions with the U.S. Department of Commerce (DOC) and the U.S. International Trade Commission (ITC) alleging that imports of seamless refined copper pipe and tube from China and Mexico (subject imports) were being sold at less than fair value and were causing material injury (and threatening material injury) to the domestic industry. On October 21, 2009, the DOC announced its decision to initiate antidumping investigations. On November 13, 2009, the ITC announced its unanimous determination that there is a reasonable indication that the domestic industry is materially injured or threatened with material injury by reason of subject imports. As a result of this preliminary determination, the DOC commenced antidumping investigations of Chinese and Mexican producers.

On May 12, 2010, the DOC published its preliminary affirmative determinations, finding antidumping rates from 29.52 percent to 30.90 percent for Mexico, and from 10.26 percent to 60.50 percent for China. As a result, U.S. importers of subject imports were required to post bonds or cash deposits at these preliminary rates. On October 1, 2010, the DOC published its final affirmative determinations, finding antidumping rates from 24.89 percent to 27.16 percent for Mexico (as amended), and from 11.25 percent to 60.85 percent for China.

On November 22, 2010, the ITC issued its final affirmative determination that subject imports from China and Mexico threatened material injury to the domestic industry. Also on November 22, 2010, the DOC published antidumping orders, with the effect that importers are required to post antidumping cash deposits at rates ranging from 24.89 percent to 27.16 percent (for subject imports from Mexico) and from 11.25 percent to 60.85 percent (for subject imports from China).

On December 22, 2010, certain Mexican parties requested panel reviews under the North American Free Trade Agreement (NAFTA) in order to appeal the ITC final determination. At this time, the Company is unable to know the final disposition of that appeal.

Employment Litigation

On June 1, 2007, the Company filed a lawsuit in the Circuit Court of Dupage County, Illinois against Peter D. Berkman and Jeffrey A. Berkman, former executives of the Company and B&K Industries, Inc. (B&K), a wholly owned subsidiary of the Company, relating to their alleged breach of fiduciary duties and contractual obligations to the Company through, among other things, their involvement with a supplier of B&K during their employment with B&K. The lawsuit alleged appropriation of corporate opportunities for personal benefit, failure to disclose competitive interests or other conflicts of interest, and unfair competition, as well as breach of employment agreements in connection with the foregoing. The lawsuit sought compensatory and punitive damages, and other appropriate relief. In August 2007, the defendants filed an answer to the complaint admitting Peter Berkman had not sought authorization to have an ownership interest in a supplier, and a counterclaim against the Company, B&K and certain of the Company’s officers and directors alleging defamation, tortious interference with prospective economic relations, and conspiracy, and seeking damages in unspecified amounts. In September 2007, Homewerks Worldwide LLC, an entity formed by Peter Berkman, filed a complaint as an intervenor based on substantially the same allegations included in the Berkmans’ counterclaim. In October 2007, the Company also filed a motion seeking to have the Berkmans’ counterclaim dismissed as a matter of law. On January 3, 2008, the Court overruled that motion and the case proceeded to discovery of the relevant facts.

On September 5, 2008, Peter Berkman withdrew prior responses to discovery requests and asserted the Fifth Amendment privilege against self-incrimination as to all requests directed to him. By that assertion, he took the position that his testimony about his actions would have the potential of exposing him to a criminal charge or criminal charges. On October 24, 2008, the defendants filed a motion seeking leave to interpose an Amended Answer and Amended Counterclaims wherein Peter Berkman asserted the Fifth Amendment in response to the allegations in the complaint. On December 19, 2008, the Company filed an answer to the Amended Counterclaims that included a new affirmative defense based on the assertion of the Fifth Amendment by Peter Berkman.

On October 3, 2008, in response to a motion to compel filed by the Company, the Court held, among other things, that Peter Berkman could not withhold documents on Fifth Amendment and attorney-client privilege grounds. Peter Berkman moved for reconsideration of that order and his request was denied on November 19, 2008. On December 10, 2008, Peter Berkman moved to file an interlocutory appeal regarding the Court’s ruling on the Company’s motion to compel. On January 7, 2009, the motion for interlocutory appeal was granted and the Court found Peter Berkman in contempt for resisting discovery. On February 6, 2009, Peter Berkman filed a notice of appeal with the Illinois Appellate Court, Second Judicial District. All appellate briefs were submitted, oral argument took place on September 29, 2009, and a publicly available decision was rendered on March 23, 2010. In that decision, the Illinois Appellate Court concluded that (i) Peter Berkman was not entitled to withhold documents on attorney-client privilege grounds that were created during the period that Katten Muchin Rosenman LLP represented both the Company and Peter Berkman, (ii) certain documents withheld on attorney-client privilege grounds needed to be submitted to the trial court for an in camera review to assess the applicability of the crime-fraud exception to the attorney-client privilege, and (iii) documents Peter Berkman withheld on Fifth Amendment grounds needed to be submitted to the trial court for an in camera review. Since obtaining this ruling, Peter Berkman unsuccessfully moved for a rehearing before the Illinois Appellate Court as to certain aspects of its decision and filed a petition for leave to appeal to the Illinois Supreme Court which was denied.

On December 15, 2009, the parties exchanged reports prepared by their respective damages experts wherein the Company asserted a claim totaling $17.2 million, not including punitive damages, and defendants asserted a claim totaling $38.0 million. The parties also exchanged rebuttal damages expert reports on March 5, 2010. The Company believed the counterclaims were without merit and defendants were not entitled to the damages being sought. Consequently, the Company intended to defend the counterclaims vigorously at trial, which was scheduled by the court to begin on January 31, 2011.

On December 10, 2010, during a pre-trial settlement conference before the court, the material terms of a settlement related to the Company’s lawsuit against Peter Berkman, Jeffrey Berkman, and Homewerks Worldwide LLC were agreed upon. On that date, the court signed an order setting forth the material terms of the settlement, which required the payment of at least $10.5 million to the Company as follows (i) the payment of $7.5 million in cash by Peter and Jeffrey Berkman to the Company; (ii) execution and delivery by Peter and Jeffrey Berkman to the Company of a promissory note in the principal amount of $3 million, secured by Peter Berkman's 70 percent interest in Homewerks Worldwide LLC; and (iii) additional future compensation. The court order also required the exchange of mutual releases. The court order did not provide for any payment by the Company, B&K, or any of their officers or directors with respect to the counterclaims.

Following the issuance of the December 10th court order, the Company further negotiated the terms of the settlement with the Berkmans and the parties agreed on the final terms of a settlement that requires the payment of $10.5 million in cash by Peter Berkman, Jeffrey Berkman, and Homewerks Worldwide LLC. This all cash payment will be made to the Company instead of the payment of $7.5 million in cash along with a promissory note in the principal amount of $3 million. Consistent with the terms of the December 10th court order, the final terms of the settlement agreement do not provide for any payment by the Company, B&K, or any of their officers or directors with respect to the counterclaims. As a result, the Company does not anticipate any material adverse effect on its financial condition, results of operations or cash flows as a result of this employment litigation matter. On February 7, 2011, the settlement agreement was executed by the parties and on February 10, 2011, the trial court dismissed with prejudice all claims and counterclaims asserted by the litigation.

PART II

|

|

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

|

As of February 21, 2011, the number of holders of record of Mueller’s common stock was approximately 1,150. On February 18, 2011, the closing price for Mueller’s common stock on the New York Stock Exchange was $33.92.

Issuer Purchases of Equity Securities

The Company’s Board of Directors has extended, until October 2011, the authorization to repurchase up to ten million shares of the Company’s common stock through open market transactions or through privately negotiated transactions. The Company has no obligation to purchase any shares and may cancel, suspend, or extend the time period for the purchase of shares at any time. Any purchases will be funded primarily through existing cash and cash from operations. The Company may hold any shares purchased in treasury or use a portion of the repurchased shares for its stock-based compensation plans, as well as for other corporate purposes. From its initial authorization in 1999 through December 25, 2010, the Company had repurchased approximately 2.4 million shares under this authorization. Below is a summary of the Company’s stock repurchases for the period ended December 25, 2010.

| |

|

(a)

|

|

|

(b)

|

|

|

(c)

|

|

|

(d)

|

|

| |

|

Total Number of Shares Purchased

|

|

|

Average Price Paid per Share

|

|

|

Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs

|

|

|

Maximum Number of Shares That May Yet Be Purchased Under the Plans or Programs

|

|

| |

|

|

|

|

|

|

|

|

|

|

7,647,030

|

(1)

|

|

September 26 – October 23, 2010

|

|

|

-

|

|

|

$

|

-

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

October 24 – November 20, 2010

|

|

|

10,906

|

|

(2)

|

|

30.53

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

November 21 – December 25, 2010

|

|

|

-

|

|

|

|

-

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1)

|

|

Shares available to be purchased under the Company's ten million share repurchase authorization until

October 2011. The extension of the authorization was announced on October 21, 2010.

|

|

(2)

|

|

Shares tendered to the Company by employee stock option holders in payment of purchase price and/or withholding taxes upon exercise.

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The Company’s Board of Directors declared a regular quarterly dividend of 10 cents per share on its common stock for each fiscal quarter of 2010 and 2009. Payment of dividends in the future is dependent upon the Company’s financial condition, cash flows, capital requirements, earnings, and other factors.

The high, low, and closing prices of Mueller's common stock on the New York Stock Exchange for each fiscal quarter of 2010 and 2009 were as follows:

| |

|

High

|

|

|

Low

|

|

|

Close

|

|

|

2010

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

Fourth quarter

|

|

$ |

33.86 |

|

|

$ |

25.23 |

|

|

$ |

33.04 |

|

|

Third quarter

|

|

|

26.29 |

|

|

|

23.10 |

|

|

|

25.90 |

|

|

Second quarter

|

|

|

31.20 |

|

|

|

23.92 |

|

|

|

24.75 |

|

|

First quarter

|

|

|

26.62 |

|

|

|

21.88 |

|

|

|

25.96 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

2009

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Fourth quarter

|

|

$ |

27.75 |

|

|

$ |

22.55 |

|

|

$ |

25.49 |

|

|

Third quarter

|

|

|

25.80 |

|

|

|

19.48 |

|

|

|

24.47 |

|

|

Second quarter

|

|

|

24.84 |

|

|

|

20.01 |

|

|

|

21.52 |

|

|

First quarter

|

|

|

26.26 |

|

|

|

16.01 |

|

|

|

22.11 |

|

PERFORMANCE GRAPH

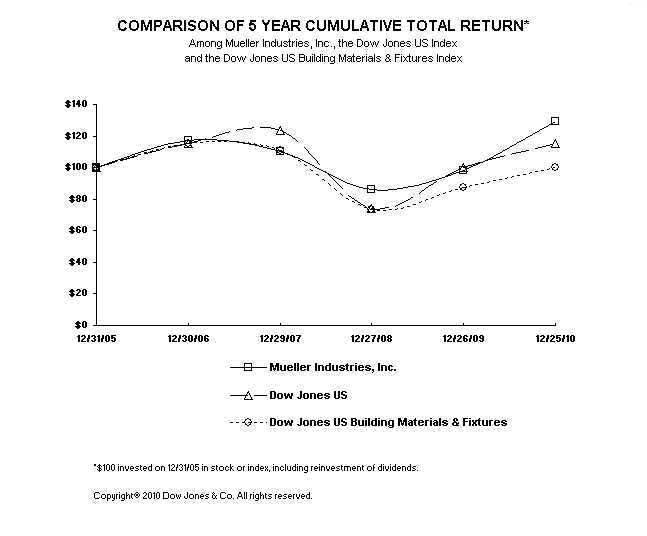

The following table compares total stockholder return since December 31, 2005 to the Dow Jones U.S. Total Market Index (Total Market Index) and the Dow Jones U.S. Building Materials & Fixtures Index (Building Materials Index). Total return values for the Total Market Index, the Building Materials Index and the Company were calculated based on cumulative total return values assuming reinvestment of dividends. The common stock is traded on the New York Stock Exchange under the symbol MLI.

| |

2005

|

2006

|

2007

|

2008

|

2009

|

2010

|

|

Mueller Industries, Inc.

|

100

|

117

|

110

|

86

|

98

|

130

|

|

Dow Jones U.S. Total Market Index

|

100

|

116

|

123

|

74

|

100

|

116

|

|

Dow Jones U.S. Building Materials & Fixtures Index

|

100

|

115

|

111

|

73

|

87

|

100

|

|

(In thousands, except per share data)

|

|

2010

|

|

|

|

|

2009

|

|

|

|

|

2008

|

|

|

|

2007

|

|

|

2006

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For the fiscal year: (1)

|

|

|

|

|