|

For

the fiscal year ended December 26, 2009

|

Commission

file number 1–6770

|

|

Delaware

|

25-0790410

|

|

(State

or other jurisdiction

|

(I.R.S.

Employer

|

|

of

incorporation or organization)

|

Identification

No.)

|

|

8285

Tournament Drive, Suite 150

|

|

|

Memphis,

Tennessee

|

38125

|

|

(Address

of principal executive offices)

|

(Zip

Code)

|

|

Title of each class

|

Name of each exchange on which

registered

|

|

Common

Stock, $0.01 Par Value

|

New

York Stock Exchange

|

|

Large

accelerated filer S

|

Accelerated

filer £

|

|

Non-accelerated

filer £

|

Smaller

reporting company £

|

|

Page

|

|||

|

Part

I

|

|||

|

Item

1.

|

3

|

||

|

Item

1A.

|

9

|

||

|

Item

1B.

|

11

|

||

|

Item

2.

|

12

|

||

|

Item

3.

|

14

|

||

|

Item

4.

|

17

|

||

|

Part

II

|

|||

|

Item

5.

|

18

|

||

|

Item

6.

|

20

|

||

|

Item

7.

|

21

|

||

|

Item

7A.

|

21

|

||

|

Item

8.

|

21

|

||

|

Item

9.

|

21

|

||

|

Item

9A.

|

21

|

||

|

Item

9B.

|

24

|

||

|

Part

III

|

|||

|

Item

10.

|

24

|

||

|

Item

11.

|

24

|

||

|

Item

12.

|

25

|

||

|

Item

13.

|

26

|

||

|

Item

14.

|

26

|

||

|

Part

IV

|

|||

|

Item

15.

|

26

|

||

|

28

|

|||

|

F-1

|

|||

|

Location

|

Expiration Date

|

|

Port

Huron, Michigan (Local 218 I.A.M.)

|

May

1, 2010

|

|

Port

Huron, Michigan (Local 44 U.A.W.)

|

June

13, 2010

|

|

Belding,

Michigan

|

August

15, 2012

|

|

Wynne,

Arkansas

|

June

28, 2010

|

|

Fulton,

Mississippi

|

August

1, 2012

|

|

North

Wales, Pennsylvania

|

August

3, 2012

|

|

Waynesboro,

Tennessee

|

November

7, 2012

|

|

Jacksboro,

Tennessee

|

September

15, 2010

|

|

Location

|

Approximate

Property Size

|

Description

|

|||||

|

Plumbing & Refrigeration

Segment

|

|||||||

|

Fulton,

MS

|

418,000

sq. ft.

52.37

acres

|

Copper

tube mill. Facility includes casting, extruding, and finishing

equipment to produce copper tubing, including tube feedstock for the

Company’s copper fittings plants and Precision Tube

factory.

|

|||||

|

Fulton,

MS

|

103,000

sq. ft.

11.9

acres

|

Casting

facility. Facility includes casting equipment to produce copper

billets used in the adjoining copper tube mill.

|

|||||

|

Wynne,

AR

|

682,000

sq. ft.

39.2

acres

|

(1)

|

Copper

tube mill and plastic fittings plant. Facility includes

casting, extruding, and finishing equipment to produce copper tubing and

copper tube line sets, and produces DWV fittings using injection molding

equipment.

|

||||

|

Fulton,

MS

|

58,500

sq. ft.

15.53

acres

|

Packaging

and bar coding facility for retail channel sales.

|

|||||

|

Fulton,

MS

|

70,000

sq. ft.

7.68

acres

|

(2)

|

Copper

fittings plant. High-volume facility that produces copper

fittings using tube feedstock from the Company’s adjacent copper tube

mill.

|

||||

|

Covington,

TN

|

159,500

sq. ft.

40.88

acres

|

Copper

fittings plant. Facility produces copper fittings using tube

feedstock from the Company’s copper tube mills.

|

|||||

|

Ontario,

CA

|

211,000

sq. ft.

10

acres

|

(3)

|

Distribution

center and plastics manufacturing plant. Produces DWV fittings

using injection molding equipment and ABS plastic pipe using pipe

extruders.

|

||||

|

Fort

Pierce, FL

|

69,875

sq. ft.

5.60

acres

|

Plastic

fittings plant. Produces pressure fittings using injection

molding equipment.

|

|||||

|

Monterrey,

Mexico

|

120,000

sq. ft.

3.4

acres

|

(3)

|

Pipe

nipples plant. Produces pipe nipples, cut pipe and merchant

couplings.

|

||||

|

Bilston,

England, United Kingdom

|

402,500

sq. ft.

14.95

acres

|

Copper

tube mill. Facility includes casting, extruding, and finishing

equipment to produce copper tubing.

|

|||||

|

(continued)

|

||||||

|

Location

|

Approximate

Property Size

|

Description

|

||||

|

OEM Segment

|

||||||

|

Port

Huron, MI

|

322,500

sq. ft.

71.5

acres

|

Brass

rod mill. Facility includes casting, extruding, and finishing

equipment to produce brass rods and bars, in various shapes and

sizes.

|

||||

|

Belding,

MI

|

293,068

sq. ft.

17.64

acres

|

Brass

rod mill. Facility includes casting, extruding, and finishing

equipment to produce brass rods and bars, in various shapes and

sizes.

|

||||

|

Port

Huron, MI

|

127,500

sq. ft.

|

Forgings

plant. Produces brass and aluminum forgings.

|

||||

|

Marysville,

MI

|

81,500

sq. ft.

6.72

acres

|

Aluminum

and copper impacts plant. Produces made-to-order parts using

cold impact processes.

|

||||

|

Hartsville,

TN

|

78,000

sq. ft.

4.51

acres

|

Refrigeration

products plant. Produces products used in refrigeration

applications such as ball valves, line valves, and compressor

valves.

|

||||

|

Carthage,

TN

|

67,520

sq. ft.

10.98

acres

|

Fabrication

facility. Produces precision tubular components and

assemblies.

|

||||

|

Waynesboro,

TN

|

57,000

sq. ft.

5.0

acres

|

(4)

|

Gas

valve plant. Facility produces brass valves and assemblies for

the gas appliance industry.

|

|||

|

North

Wales, PA

|

174,000

sq. ft.

18.9

acres

|

Precision

Tube factory. Facility fabricates copper tubing, copper alloy

tubing, aluminum tubing, and fabricated tubular

products.

|

||||

|

Brighton,

MI

|

65,000 sq.

ft.

|

(3)

|

Machining

operation. Facility machines component parts for supply to

automotive industry.

|

|||

|

Middletown,

OH

|

55,000

sq. ft.

2.0

acres

|

Fabricating

facility. Produces burner systems and manifolds for the gas

appliance industry.

|

||||

|

Jintan

City, Jiangsu Province, China

|

322,580 sq.

ft

33.0

acres

|

(5)

|

Copper

tube mill. Facility includes casting, and finishing equipment

to produce engineered copper tube primarily for

OEMs.

|

|||

|

(1)

|

Facility,

or some portion thereof, is located on land leased from a local

municipality, with an option to purchase at nominal

cost.

|

|

(2)

|

Facility

is leased under a long-term lease agreement, with an option to purchase at

nominal cost.

|

|

(3)

|

Facility

is leased under an operating lease.

|

|

(4)

|

Facility

is leased from a local municipality for a nominal

amount.

|

|

(5)

|

Facility

is located on land that is under a long-term land use rights

agreement.

|

|

(a)

|

(b)

|

(c)

|

(d)

|

|||||||||||||||

|

Total Number

of Shares Purchased

|

Average

Price Paid per Share

|

Total

Number of Shares Purchased as Part of Publicly Announced Plans or

Programs

|

Maximum

Number of Shares That May Yet Be Purchased Under the Plans or

Programs

|

|||||||||||||||

|

7,647,030

|

(1)

|

|||||||||||||||||

|

September

27 – October 24, 2009

|

-

|

$

|

-

|

|||||||||||||||

|

October

25 – November 21, 2009

|

8,068

|

(2)

|

26.01

|

|||||||||||||||

|

November

22 – December 26, 2009

|

9,879

|

(2)

|

24.67

|

|||||||||||||||

|

(1

|

)

|

Shares

available to be purchased under the Company's 10 million share repurchase

authorization until October 2010. The extension of the

authorization was announced on October 21, 2009.

|

||||||||||||||||

|

(2

|

)

|

Shares

tendered to the Company by employee stock option holders in payment of

purchase price and/or withholding taxes upon exercise.

|

||||||||||||||||

|

High

|

Low

|

Close

|

||||||||||

|

2009

|

||||||||||||

|

Fourth

quarter

|

$ | 27.75 | $ | 22.55 | $ | 25.49 | ||||||

|

Third

quarter

|

25.80 | 19.48 | 24.47 | |||||||||

|

Second

quarter

|

24.84 | 20.01 | 21.52 | |||||||||

|

First

quarter

|

26.26 | 16.01 | 22.11 | |||||||||

|

2008

|

||||||||||||

|

Fourth

quarter

|

$ | 26.28 | $ | 15.69 | $ | 22.81 | ||||||

|

Third

quarter

|

33.33 | 24.85 | 26.83 | |||||||||

|

Second

quarter

|

36.73 | 28.49 | 32.29 | |||||||||

|

First

quarter

|

31.21 | 23.57 | 29.43 | |||||||||

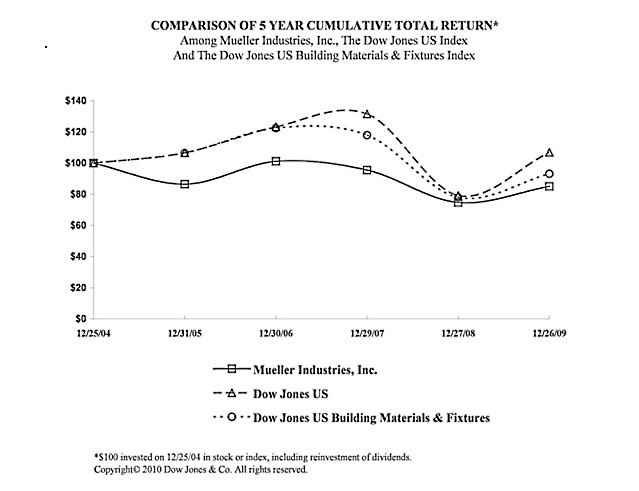

|

2004

|

2005

|

2006

|

2007

|

2008

|

2009

|

|

|

Mueller

Industries, Inc.

|

100

|

86

|

101

|

96

|

75

|

85

|

|

Dow

Jones U.S. Total Market Index

|

100

|

107

|

123

|

131

|

79

|

107

|

|

Dow

Jones U.S. Building Materials & Fixtures Index

|

100

|

106

|

122

|

118

|

78

|

93

|

|

(In

thousands, except per share data)

|

|||||||||||||||||||||||||||||

|

2009

|

2008

|

2007

|

2006

|

2005

|

|||||||||||||||||||||||||

|

For

the fiscal year: (1)

|

|||||||||||||||||||||||||||||

|

Net

sales

|

$

|

1,547,225

|

$

|

2,558,448

|

$

|

2,697,845

|

$

|

2,510,912

|

$

|

1,729,923

|

|||||||||||||||||||

|

Operating

income

|

32,220

|

(7

|

)

|

126,096

|

(5

|

)

|

191,621

|

(4

|

)

|

218,885

|

(2

|

)

|

131,758

|

||||||||||||||||

|

|

|||||||||||||||||||||||||||||

|

Net

income from continuing operations attributable to Mueller Industries,

Inc.

|

4,675

|

80,814

|

(6

|

)

|

115,475

|

148,869

|

(3

|

)

|

89,218

|

||||||||||||||||||||

|

Diluted

earnings per share from continuing operations

|

0.12

|

2.17

|

3.10

|

4.00

|

2.40

|

||||||||||||||||||||||||

|

Cash

dividends per share

|

0.40

|

0.40

|

0.40

|

0.40

|

0.40

|

||||||||||||||||||||||||

|

At

year-end:

|

|||||||||||||||||||||||||||||

|

Total

assets

|

1,180,141

|

1,182,913

|

1,449,204

|

1,268,907

|

1,116,928

|

||||||||||||||||||||||||

|

Long-term

debt

|

158,226

|

158,726

|

281,738

|

308,154

|

312,070

|

||||||||||||||||||||||||

| (1 | ) |

|

Includes

activity of acquired businesses from the following purchase dates: (i)

Extruded, February 27, 2007, (ii) Mueller-Xingrong, December 2005, and

(iii) Brassware, August 15, 2005.

|

||||||||||||||||||||||||||

| (2 | ) |

|

In

2006, the Company recorded a pre-tax charge of $14.2 million to write down

inventories to the lower-of-cost-or-market.

|

||||||||||||||||||||||||||

| (3 | ) |

|

Includes

the net-of-tax effect of the inventory write-down described in (2) above,

plus a $7.7 million benefit for change in estimate regarding the future

utilization of various tax incentives in 2006.

|

||||||||||||||||||||||||||

| (4 | ) |

|

Includes

$10.0 million pre-tax gain from liquidation of LIFO layers plus a gain

from a copper litigation settlement of $8.9 million, less a goodwill

impairment charge of $2.8 million.

|

||||||||||||||||||||||||||

| (5 | ) |

|

Includes

$14.9 million pre-tax gain from liquidation of LIFO layers less a pre-tax

charge of $4.9 million to write down inventories to the

lower-of-cost-or-market and a goodwill impairment charge of $18.0

million.

|

||||||||||||||||||||||||||

| (6 | ) |

|

Includes

the net-of-tax effect of all of the items described in (5) above, plus a

provision of $15.4 million ($9.6 million after tax) related to

environmental settlements and obligations and a gain of $21.6 million

related to the early extinguishment of debt.

|

||||||||||||||||||||||||||

| (7 | ) |

|

Includes

impairment charges of $29.8 million, primarily related to

goodwill.

|

||||||||||||||||||||||||||

| /S/ Ernst & Young LLP |

|

Memphis,

Tennessee

|

|

|

February

23, 2010

|

|

(a)

|

(b)

|

(c)

|

||||||||||

|

Plan

category

|

Number

of securities to be issued upon exercise of outstanding options, warrants,

and rights

|

Weighted

average exercise price of outstanding options, warrants, and

rights

|

Number

of securities remaining available for future issuance under equity

compensation plans (excluding securities reflected in column

(a))

|

|||||||||

|

Equity

compensation plans approved by security holders

|

1,604 | $ | 27.56 | 992 | ||||||||

|

Equity

compensation plans not approved by security holders

|

— | — | — | |||||||||

|

Total

|

1,604 | $ | 27.56 | 992 | ||||||||

|

(a)

|

The

following documents are filed as part of this report:

|

|

|

1.

|

Financial

Statements: the financial statements, notes, and report of independent

registered public accounting firm described in Item 8 of this Annual

Report on Form 10-K are contained in a separate section of this Annual

Report on Form 10-K commencing on page F-1.

|

|

|

2.

|

Financial

Statement Schedule: the financial statement schedule described in Item 8

of this report is contained in a separate section of this Annual Report on

Form 10-K commencing on page F-1.

|

|

|

3.

|

Exhibits:

|

|

|

3.1

|

Restated

Certificate of Incorporation of the Registrant dated February 8, 2007

(Incorporated herein by reference to Exhibit 3.1 of the Registrant’s

Annual Report on Form 10-K, dated February 28, 2007, for the fiscal year

ended December 30, 2006).

|

|

|

3.2

|

Amended

and Restated By-laws of the Registrant, adopted and effective as of July

30, 2009 (Incorporated herein by reference to Exhibit 3.1 of the

Registrant’s Current Report on Form 8 - K, dated July 30,

2009).

|

|

|

4.1

|

Indenture,

dated as of October 26, 2004, by and between Mueller Industries, Inc, and

SunTrust Bank, as trustee (Incorporated herein by reference to Exhibit 4.1

of the Registrant’s Current Report on Form 8-K, dated October 26,

2004).

|

|

|

4.2

|

Form

of 6% Subordinated Debenture due 2014 (Incorporated herein by reference to

Exhibit 4.2 of the Registrant’s Current Report on Form 8-K, dated October

26, 2004).

|

|

|

4.3

|

Certain

instruments with respect to long-term debt of the Registrant have not been

filed as Exhibits to this Report since the total amount of securities

authorized under any such instruments does not exceed 10 percent of the

total assets of the Registrant and its subsidiaries on a consolidated

basis. The Registrant agrees to furnish a copy of each such

instrument upon request of the SEC.

|

|

|

10.1

|

Amended

and Restated Employment Agreement, effective as of September 17, 1997, by

and between the Registrant and Harvey L. Karp (Incorporated herein by

reference to Exhibit 10.8 of the Registrant’s Annual Report on Form 10-K,

dated March 24, 2003, for the fiscal year ended December 28,

2002).

|

|

|

10.2

|

Amendment,

dated June 21, 2004, to the Amended and Restated Employment Agreement

dated as of September 17, 1997, by and between the Registrant and Harvey

Karp (Incorporated herein by reference to Exhibit 10.3 of the Registrant’s

Quarterly Report on Form 10-Q, dated July 16, 2004, for the quarter ended

June 26, 2004).

|

|

|

10.3

|

Second

Amendment, dated February 17, 2005, to the Amended and Restated Employment

Agreement, dated as of September 17, 1997, between the Registrant and

Harvey Karp (Incorporated herein by reference to Exhibit 10.2 of the

Registrant’s Current Report on Form 8-K, dated May 5,

2005).

|

|

|

10.4

|

Third

Amendment, dated October 25, 2007, to the Amended and Restated Employment

Agreement, dated as of September 17, 1997, by and between the Registrant

and Harvey Karp (Incorporated herein by reference to Exhibit 10.1 of the

Registrant’s Current Report on Form 8-K, dated October 25,

2007).

|

|

|

10.5

|

Fourth

Amendment, dated December 2, 2008, to the Amended and Restated Employment

Agreement, dated as of September 17, 1997, by and between the Registrant

and Harvey Karp (Incorporated herein by reference to Exhibit 10.5 of the

Registrant's Annual Report on Form 10-K, dated February 24, 2009, for the

fiscal year ended December 27, 2008).

|

|

|

10.6

|

Amended

and Restated Consulting Agreement, dated October 25, 2007, by and between

the Registrant and Harvey Karp (Incorporated herein by reference to

Exhibit 10.2 of the Registrant’s Current Report on Form 8-K, dated October

25, 2007).

|

|

|

10.7

|

Amendment

No. 1, dated December 2, 2008, to the Amended and Restated Consulting

Agreement, dated October 25, 2007, by and between the Registrant and

Harvey Karp (Incorporated herein by reference to Exhibit 10.7 of the

Registrant's Annual Report on Form 10-K, dated February 24, 2009, for the

fiscal year ended December 27, 2008).

|

|

|

10.8

|

Employment

Agreement, effective October 17, 2002, by and between the Registrant and

Kent A. McKee (Incorporated herein by reference to Exhibit 10.18 of the

Registrant’s Annual Report on Form 10-K, dated March 24, 2003, for the

fiscal year ended December 28, 2002).

|

|

|

10.9

|

Amendment

No. 1, dated December 10, 2008, to the Employment Agreement, effective

October 17, 2002, by and between the Registrant and Kent A. McKee

(Incorporated herein by reference to Exhibit 10.16 of the Registrant's

Annual Report on Form 10-K, dated February 24, 2009, for the fiscal year

ended December 27, 2008).

|

|

|

10.10

|

Amended

and Restated Employment Agreement, effective October 30, 2008, by and

between the Registrant and Gregory L. Christopher (Incorporated herein by

reference to Exhibit 10.1 of the Registrant’s Current Report on Form 8-K,

dated December 26, 2008).

|

|

|

10.11

|

Mueller

Industries, Inc. 1991 Incentive Stock Option Plan, as amended

(Incorporated herein by reference to Exhibit 10.6 of the Registrant’s

Annual Report on Form 10-K, dated March 24, 2003, for the fiscal year

ended December 28, 2002 and Exhibit 99.2 of the Registrant’s Current

Report on Form 8-K, dated August 31, 2004).

|

|

|

10.12

|

Mueller

Industries, Inc. 1994 Stock Option Plan, as amended (Incorporated herein

by reference to Exhibit 10.11 of the Registrant’s Annual Report on Form

10-K, dated March 24, 2003, for the fiscal year ended December 28, 2002

and Exhibit 99.3 of the Registrant’s Current Report on Form 8-K, dated

August 31, 2004).

|

|

|

10.13

|

Mueller

Industries, Inc. 1994 Non-Employee Director Stock Option Plan, as amended

(Incorporated herein by reference to Exhibit 10.12 of the Registrant’s

Annual Report on Form 10-K, dated March 24, 2003, for the fiscal year

ended December 28, 2002 and Exhibit 99.6 of the Registrant’s Current

Report on Form 8-K, dated August 31, 2004).

|

|

|

10.14

|

Mueller

Industries, Inc. 1998 Stock Option Plan, as amended (Incorporated herein

by reference to Exhibit 10.14 of the Registrant’s Annual Report on Form

10-K, dated March 24, 2003, for the fiscal year ended December 28, 2002

and Exhibit 99.4 of the Registrant’s Current Report on Form 8-K, dated

August 31, 2004).

|

|

|

10.15

|

Mueller

Industries, Inc. 2002 Stock Option Plan Amended and Restated as of

February 16, 2006 (Incorporated herein by reference to Exhibit 10.20 of

the Registrant’s Annual Report on Form 10-K, dated February 28, 2007, for

the fiscal year ended December 30, 2006).

|

|

|

10.16

|

Mueller

Industries, Inc. 2009 Stock Incentive Plan (Incorporated by reference from

Appendix I to the Company’s 2009 Definitive Proxy Statement with respect

to the Company’s 2009 Annual Meeting of Stockholders, as filed with the

Securities and Exchange Commission on March 26, 2009).

|

|

|

10.17

|

Mueller

Industries, Inc. Annual Bonus Plan (Incorporated herein by reference to

Exhibit 10.1 of the Registrant’s Current Report on Form 8-K, dated May 5,

2005).

|

|

|

10.18

|

Summary

description of the Registrant’s 2010 incentive plan for certain key

employees.

|

|

|

10.19

|

Credit

Agreement, dated as of December 1, 2006, among the Registrant (as

Borrower) and Lasalle Bank Midwest National Association (as agent), and

certain lenders named therein (Incorporated herein by reference to Exhibit

10.1 of the Registrant’s Current Report on Form 8-K, dated December 1,

2006).

|

|

|

10.20

|

Equity

Joint Venture Agreement, among Mueller Streamline China, LLC, Mueller

Streamline Holding, S.L., Jiangsu Xingrong Hi-Tech Co., Ltd. and Jiangsu

Baiyang Industries Ltd. (Incorporated herein by reference to Exhibit 10.1

of the Registrant’s Current Report on Form 8-K, dated December 5,

2005).

|

|

|

21.0

|

Subsidiaries

of the Registrant.

|

|

|

23.0

|

Consent

of Independent Registered Public Accounting Firm.

|

|

|

31.1

|

Certification

of Chief Executive Officer pursuant to Rule 13a-14(a) and Rule 15d-14(a)

of the Securities Exchange Act of 1934, as amended.

|

|

|

31.2

|

Certification

of Chief Financial Officer pursuant to Rule 13a-14(a) and Rule 15d-14(a)

of the Securities Exchange Act of 1934, as amended.

|

|

|

32.1

|

Certification

of Chief Executive Officer pursuant to 18 U.S.C. 1350, as adopted pursuant

to Section 906 of the Sarbanes-Oxley Act of 2002.

|

|

|

32.2

|

Certification

of Chief Financial Officer pursuant to 18 U.S.C. 1350, as adopted pursuant

to Section 906 of the Sarbanes-Oxley Act of

2002.

|

|

/S/

Harvey L.

Karp

|

||

|

Harvey

L. Karp, Chairman of the Board

|

|

Signature

|

Title

|

Date

|

|

/S/ Harvey L

Karp

|

Chairman

of the Board, and Director

|

February 23,

2010

|

|

Harvey

L. Karp

|

||

|

/S/Alexander P.

Federbush

|

Director

|

February 23,

2010

|

|

Alexander

P. Federbush

|

||

|

/S/

Paul

J. Flaherty

|

Director

|

February

23, 2010

|

|

Paul

J. Flaherty

|

||

|

/S/ Gennaro J.

Fulvio

|

Director

|

February

23, 2010

|

|

Gennaro

J. Fulvio

|

||

|

/S/ Gary S.

Gladstein

|

Director

|

February

23, 2010

|

|

Gary

S. Gladstein

|

||

|

/S/ Scott J.

Goldman

|

Director

|

February

23, 2010

|

|

Scott

J. Goldman

|

||

|

/S/ Terry

Hermanson

|

Director

|

February

23, 2010

|

|

Terry

Hermanson

|

|

Signature and Title

|

Date

|

|

|

/S/ Gregory L. Christopher

|

February

23, 2010

|

|

|

Gregory

L. Christopher

|

||

|

Chief

Executive Officer

|

||

|

(Principal

Executive Officer)

|

||

|

/S/ Kent A.

McKee

|

February

23, 2010

|

|

|

Kent

A. McKee

|

||

|

Executive

Vice President and Chief Financial Officer

|

||

|

(Principal

Financial and Accounting Officer)

|

||

|

/S/ Richard W.

Corman

|

February

23, 2010

|

|

|

Richard

W. Corman

|

||

|

Vice

President – Controller

|

|

F-

2

|

|

|

F-

12

|

|

|

F-

13

|

|

|

F-

14

|

|

|

F-

15

|

|

|

F-

17

|

|

|

F-

47

|

|

|

Schedule

for the years ended December 26, 2009, December 27, 2008, and December 29,

2007

|

|

|

F-

48

|

|

|

Payments

Due by Year

|

|||||||||||||||||||||

|

(In

millions)

|

Total

|

2010

|

2011-2012

|

2013-2014

|

Thereafter

|

||||||||||||||||

|

Debt

|

$

|

182.6

|

$

|

24.3

|

$

|

1.8

|

$

|

150.2

|

$

|

6.3

|

|||||||||||

|

Interest

on fixed rate debt

|

44.5

|

8.9

|

17.8

|

17.8

|

—

|

||||||||||||||||

|

Consulting

Agreement (1)

|

6.7

|

1.3

|

2.7

|

2.0

|

0.7

|

||||||||||||||||

|

Operating

leases

|

31.6

|

6.3

|

9.6

|

5.9

|

9.8

|

||||||||||||||||

|

Purchase

commitments (2)

|

130.0

|

130.0

|

—

|

—

|

—

|

||||||||||||||||

|

Total

contractual cash obligations

|

$

|

395.4

|

$

|

170.8

|

$

|

31.9

|

$

|

175.9

|

$

|

16.8

|

|||||||||||

|

(1)

|

See

Note 10 to Consolidated Financial Statements. For the purposes

of this disclosure, the Company assumed the Consulting Agreement is

effective immediately.

|

||||||||||||||||||||

|

(2)

|

Purchase

commitments included $7.4 million of open fixed price purchases of raw

materials. Additionally, the Company has contractual supply

commitments for raw materials totaling $116.2 million at year end prices;

these contracts contain variable pricing based on Comex and the London

Metals Exchange (LME). These commitments are for purchases of

raw materials that are expected to be consumed in the ordinary course of

business.

|

||||||||||||||||||||

|

(In

thousands, except per share data)

|

2009

|

2008

|

2007

|

|||||||||

|

Net

sales

|

$

|

1,547,225

|

$

|

2,558,448

|

$

|

2,697,845

|

||||||

|

Cost

of goods sold

|

1,327,022

|

2,233,123

|

2,324,924

|

|||||||||

|

Depreciation

and amortization

|

41,568

|

44,345

|

44,153

|

|||||||||

|

Selling,

general, and administrative expense

|

116,660

|

136,884

|

143,284

|

|||||||||

|

Copper

litigation settlement

|

—

|

—

|

(8,893

|

)

|

||||||||

|

Impairment

charges

|

29,755

|

18,000

|

2,756

|

|||||||||

|

Operating

income

|

32,220

|

126,096

|

191,621

|

|||||||||

|

Interest

expense

|

(9,963

|

)

|

(19,050

|

)

|

(22,071

|

)

|

||||||

|

Other

income, net

|

872

|

13,896

|

14,313

|

|||||||||

|

Income

before income taxes

|

23,129

|

120,942

|

183,863

|

|||||||||

|

Income

tax expense

|

(17,792

|

)

|

(38,332

|

)

|

(67,806

|

)

|

||||||

|

Consolidated

net income

|

5,337

|

82,610

|

116,057

|

|||||||||

|

Less

net income attributable to noncontrolling interest

|

(662

|

)

|

(1,796

|

)

|

(582

|

)

|

||||||

|

Net

income attributable to Mueller Industries, Inc.

|

$

|

4,675

|

$

|

80,814

|

$

|

115,475

|

||||||

|

Weighted

average shares for basic earnings per share

|

37,336

|

37,123

|

37,060

|

|||||||||

|

Effect

of dilutive stock-based awards

|

88

|

186

|

163

|

|||||||||

|

Adjusted

weighted average shares for diluted earnings per share

|

37,424

|

37,309

|

37,223

|

|||||||||

|

Basic

earnings per share

|

$

|

0.13

|

$

|

2.18

|

$

|

3.12

|

||||||

|

Diluted

earnings per share

|

$

|

0.12

|

$

|

2.17

|

$

|

3.10

|

||||||

|

Dividends

per share

|

$

|

0.40

|

$

|

0.40

|

$

|

0.40

|

||||||

|

See

accompanying notes to consolidated financial statements.

|

||||||||||||

|

(In

thousands, except share data)

|

2009

|

2008

|

||||||

|

Assets

|

||||||||

|

Current

assets:

|

||||||||

|

Cash

and cash equivalents

|

$

|

346,001

|

$

|

278,860

|

||||

|

Accounts receivable, less allowance for doubtful accounts of $5,947 in

2009 and $6,690 in 2008

|

228,739

|

219,035

|

||||||

|

Inventories

|

191,262

|

210,609

|

||||||

|

Current

deferred income taxes

|

18,491

|

17,212

|

||||||

|

Other

current assets

|

24,350

|

29,110

|

||||||

|

Total

current assets

|

808,843

|

754,826

|

||||||

|

Property,

plant, and equipment, net

|

250,395

|

276,927

|

||||||

|

Goodwill

|

102,250

|

129,186

|

||||||

|

Other

assets

|

18,653

|

21,974

|

||||||

|

Total

Assets

|

$

|

1,180,141

|

$

|

1,182,913

|

||||

|

Liabilities

|

||||||||

|

Current

liabilities:

|

||||||||

|

Current

portion of debt

|

$

|

24,325

|

$

|

24,184

|

||||

|

Accounts

payable

|

73,837

|

63,732

|

||||||

|

Accrued

wages and other employee costs

|

24,829

|

35,079

|

||||||

|

Other

current liabilities

|

60,379

|

78,589

|

||||||

|

Total

current liabilities

|

183,370

|

201,584

|

||||||

|

Long-term

debt, less current portion

|

158,226

|

158,726

|

||||||

|

Pension

liabilities

|

20,715

|

13,903

|

||||||

|

Postretirement

benefits other than pensions

|

23,605

|

24,549

|

||||||

|

Environmental

reserves

|

23,268

|

23,248

|

||||||

|

Deferred

income taxes

|

31,128

|

33,940

|

||||||

|

Other

noncurrent liabilities

|

887

|

1,698

|

||||||

|

Total

liabilities

|

441,199

|

457,648

|

||||||

|

Equity

|

||||||||

|

Mueller

Industries, Inc. stockholders' equity:

|

||||||||

|

Preferred

stock - $1.00 par value; shares authorized 5,000,000; none

outstanding

|

—

|

—

|

||||||

|

Common stock - $.01 par value; shares authorized 100,000,000; issued

40,091,502; outstanding 37,649,584 in 2009 and 37,143,163 in

2008

|

401

|

401

|

||||||

|

Additional

paid-in capital

|

262,166

|

262,378

|

||||||

|

Retained

earnings

|

540,218

|

550,501

|

||||||

|

Accumulated

other comprehensive loss

|

(36,104

|

)

|

(48,113

|

)

|

||||

|

Treasury

common stock, at cost

|

(53,514

|

)

|

(64,484

|

)

|

||||

|

Total

Mueller Industries, Inc. stockholders' equity

|

713,167

|

700,683

|

||||||

|

Noncontrolling

interest

|

25,775

|

24,582

|

||||||

|

Total

equity

|

738,942

|

725,265

|

||||||

|

Commitments

and contingencies

|

—

|

—

|

||||||

|

Total

Liabilities and Equity

|

$

|

1,180,141

|

$

|

1,182,913

|

||||

|

See

accompanying notes to consolidated financial statements.

|

||||||||

|

(In

thousands)

|

2009

|

2008

|

2007

|

|||||||||

|

Operating

activities:

|

||||||||||||

|

Net

income attributable to Mueller Industries, Inc.

|

$

|

4,675

|

$

|

80,814

|

$

|

115,475

|

||||||

|

Reconciliation

of net income attributable to Mueller Industries, Inc. to net cash

provided by operating activities:

|

||||||||||||

|

Depreciation

|

40,867

|

43,666

|

43,605

|

|||||||||

|

Amortization

of intangibles

|

701

|

679

|

548

|

|||||||||

|

Amortization

of Subordinated Debenture costs

|

190

|

539

|

324

|

|||||||||

|

Stock-based

compensation expense

|

2,633

|

2,915

|

2,737

|

|||||||||

|

Income

tax benefit from exercise of stock options

|

(203

|

)

|

(92

|

)

|

(73

|

)

|

||||||

|

Impairment

charges

|

29,755

|

18,000

|

2,756

|

|||||||||

|

Deferred

income taxes

|

(2,554

|

)

|

(4,465

|

)

|

3,094

|

|||||||

|

Provision

for doubtful accounts receivable

|

506

|

2,654

|

(177

|

)

|

||||||||

|

Net

income attributable to noncontrolling interest

|

662

|

1,796

|

582

|

|||||||||

|

Gain

on early retirement of debt

|

(128

|

)

|

(21,575

|

)

|

—

|

|||||||

|

Loss

(gain) on disposal of properties

|

683

|

598

|

(2,468

|

)

|

||||||||

|

Changes

in assets and liabilities, net of business acquired:

|

||||||||||||

|

Receivables

|

(6,988

|

)

|

89,051

|

(7,937

|

)

|

|||||||

|

Inventories

|

22,699

|

44,591

|

20,411

|

|||||||||

|

Other

assets

|

(505

|

)

|

(3,027

|

)

|

(4,120

|

)

|

||||||

|

Current

liabilities

|

(13,823

|

)

|

(84,584

|

)

|

12,704

|

|||||||

|

Other

liabilities

|

(1,808

|

)

|

12,741

|

1,809

|

||||||||

|

Other,

net

|

26

|

1,459

|

(2,063

|

)

|

||||||||

|

Net

cash provided by operating activities

|

77,388

|

185,760

|

187,207

|

|||||||||

|

Investing

activities:

|

||||||||||||

|

Capital

expenditures

|

(13,942

|

)

|

(22,261

|

)

|

(29,870

|

)

|

||||||

|

Acquisition

of businesses, net of cash received

|

—

|

—

|

(32,243

|

)

|

||||||||

|

Proceeds

from sales of properties and equity investment

|

611

|

81

|

3,809

|

|||||||||

|

Net

withdrawals from (deposits into) restricted cash balances

|

7,013

|

(10,945

|

)

|

(4,194

|

)

|

|||||||

|

Net

cash used in investing activities

|

(6,318

|

)

|

(33,125

|

)

|

(62,498

|

)

|

||||||

|

Financing

activities:

|

||||||||||||

|

Repayments

of long-term debt

|

(370

|

)

|

(126,877

|

)

|

(18,765

|

)

|

||||||

|

Dividends

paid to stockholders of Mueller Industries, Inc.

|

(14,944

|

)

|

(14,847

|

)

|

(14,825

|

)

|

||||||

|

Dividends

paid to noncontrolling interests

|

(1,449

|

)

|

—

|

(1,363

|

)

|

|||||||

|

Issuance

(repayment) of debt by joint venture, net

|

131

|

(25,564

|

)

|

16,635

|

||||||||

|

Acquisition

of treasury stock

|

(870

|

)

|

(32

|

)

|

(54

|

)

|

||||||

|

Issuance

of shares under incentive stock option plans from treasury

|

9,145

|

1,167

|

1,124

|

|||||||||

|

Income

tax benefit from exercise of stock options

|

203

|

92

|

73

|

|||||||||

|

Net

cash used in financing activities

|

(8,154

|

)

|

(166,061

|

)

|

(17,175

|

)

|

||||||

|

Effect

of exchange rate changes on cash

|

4,225

|

(16,332

|

)

|

613

|

||||||||

|

Increase

(decrease) in cash and cash equivalents

|

67,141

|

(29,758

|

)

|

108,147

|

||||||||

|

Cash

and cash equivalents at the beginning of the year

|

278,860

|

308,618

|

200,471

|

|||||||||

|

Cash

and cash equivalents at the end of the year

|

$

|

346,001

|

$

|

278,860

|

$

|

308,618

|

||||||

|

For

supplemental disclosures of cash flow information, see Notes 1, 5, 7, and

14.

|

||||||||||||

|

See

accompanying notes to consolidated financial statements.

|

||||||||||||

|

2009

|

2008

|

2007

|

||||||||||||||||||||||

|

(In

thousands)

|

Shares

|

Amount

|

Shares

|

Amount

|

Shares

|

Amount

|

||||||||||||||||||

|

Common

stock:

|

||||||||||||||||||||||||

|

Balance

at beginning of year

|

40,092

|

$

|

401

|

40,092

|

$

|

401

|

40,092

|

$

|

401

|

|||||||||||||||

|

Balance

at end of year

|

40,092

|

$

|

401

|

40,092

|

$

|

401

|

40,092

|

$

|

401

|

|||||||||||||||

|

Additional

paid-in capital:

|

||||||||||||||||||||||||

|

Balance

at beginning of year

|

$

|

262,378

|

$

|

259,611

|

$

|

256,906

|

||||||||||||||||||

|

Issuance

of shares under incentive stock option plans

|

(1,295

|

)

|

(240

|

)

|

(105

|

)

|

||||||||||||||||||

|

Stock-based

compensation expense

|

2,633

|

2,915

|

2,737

|

|||||||||||||||||||||

|

Income

tax benefit from exercise of stock options

|

203

|

92

|

73

|

|||||||||||||||||||||

|

Write-off

of excess tax benefits arising from the exercise of stock

options

|

(353

|

)

|

—

|

—

|

||||||||||||||||||||

|

Issuance

of restricted stock

|

(1,400

|

)

|

—

|

—

|

||||||||||||||||||||

|

Balance

at end of year

|

$

|

262,166

|

$

|

262,378

|

$

|

259,611

|

||||||||||||||||||

|

Retained

earnings:

|

||||||||||||||||||||||||

|

Balance

at beginning of year

|

$

|

550,501

|

$

|

484,534

|

$

|

386,038

|

||||||||||||||||||

|

Adjustment

to retained earnings due to the adoption of the provisions for uncertain

tax positions codified in ASC 740

|

—

|

—

|

(2,154

|

)

|

||||||||||||||||||||

|

Net

income attributable to Mueller Industries, Inc.

|

4,675

|

80,814

|

115,475

|

|||||||||||||||||||||

|

Dividends

paid or payable to stockholders of Mueller Industries,

Inc.

|

(14,958

|

)

|

(14,847

|

)

|

(14,825

|

)

|

||||||||||||||||||

|

Balance

at end of year

|

$

|

540,218

|

$

|

550,501

|

$

|

484,534

|

||||||||||||||||||

|

Accumulated

other comprehensive (loss) income:

|

||||||||||||||||||||||||

|

Foreign

currency translation

|

$

|

13,278

|

$

|

(51,701

|

)

|

$

|

4,606

|

|||||||||||||||||

|

Net

change with respect to derivative instruments and hedging activities, net

of tax of $(1,794), $1,347, and $(166)

|

4,097

|

(3,819

|

)

|

285

|

||||||||||||||||||||

|

Net

actuarial (loss) gain on pension and postretirement obligations, net of

tax of $2,138, $14,867 and $(7,116)

|

(5,655

|

)

|

(26,542

|

)

|

14,170

|

|||||||||||||||||||

|

Other,

net

|

289

|

2,141

|

244

|

|||||||||||||||||||||

|

Total

other comprehensive income (loss) attributable to Mueller Industries,

Inc.

|

12,009

|

(79,921

|

)

|

19,305

|

||||||||||||||||||||

|

Balance

at beginning of year

|

(48,113

|

)

|

31,808

|

12,503

|

||||||||||||||||||||

|

Balance

at end of year

|

$

|

(36,104

|

)

|

$

|

(48,113

|

)

|

$

|

31,808

|

||||||||||||||||

|

|

||||||||||||||||||||||||

|

2009

|

2008

|

2007

|

||||||||||||||||||||||

|

(In

thousands)

|

Shares

|

Amount

|

Shares

|

Amount

|

Shares

|

Amount

|

||||||||||||||||||

|

Treasury

stock:

|

||||||||||||||||||||||||

|

Balance

at beginning of year

|

2,949

|

$

|

(64,484

|

)

|

3,012

|

$

|

(65,859

|

)

|

3,067

|

$

|

(67,034

|

)

|

||||||||||||

|

Issuance

of shares under incentive stock option plans

|

(477

|

)

|

10,440

|

(65

|

)

|

1,407

|

(57

|

)

|

1,229

|

|||||||||||||||

|

Repurchase

of common stock

|

34

|

(870

|

)

|

2

|

(32

|

)

|

2

|

(54

|

)

|

|||||||||||||||

|

Issuance

of restricted stock

|

(64

|

)

|

1,400

|

—

|

—

|

—

|

—

|

|||||||||||||||||

|

Balance

at end of year

|

2,442

|

$

|

(53,514

|

)

|

2,949

|

$

|

(64,484

|

)

|

3,012

|

$

|

(65,859

|

)

|

||||||||||||

|

|

||||||||||||||||||||||||

|

Noncontrolling

interest:

|

||||||||||||||||||||||||

|

Balance

at beginning of year

|

$

|

24,582

|

$

|

22,765

|

$

|

22,300

|

||||||||||||||||||

|

Net

income attributable to noncontrolling interest

|

662

|

1,796

|

582

|

|||||||||||||||||||||

|

Sale

of noncontrolling interests

|

—

|

—

|

(77

|

)

|

||||||||||||||||||||

|

Dividends

paid to noncontrolling interests

|

(1,449

|

)

|

—

|

(1,363

|

)

|

|||||||||||||||||||

|

Net

change with respect to derivative instruments and hedging activities, net

of tax of $(279) and $279

|

1,952

|

(1,952

|

)

|

—

|

||||||||||||||||||||

|

Foreign

currency translation

|

28

|

1,973

|

1,323

|

|||||||||||||||||||||

|

Balance

at end of year

|

$

|

25,775

|

$

|

24,582

|

$

|

22,765

|

||||||||||||||||||

|

Comprehensive

income:

|

||||||||||||||||||||||||

|

Consolidated

net income

|

$

|

5,337

|

$

|

82,610

|

$

|

116,057

|

||||||||||||||||||

|

Consolidated

other comprehensive income (loss)

|

13,989

|

(79,900

|

)

|

20,628

|

||||||||||||||||||||

|

Consolidated

comprehensive income

|

19,326

|

2,710

|

136,685

|

|||||||||||||||||||||

|

Less:

comprehensive income attributable to noncontrolling

interest

|

(2,642

|

)

|

(1,817

|

)

|

(1,905

|

)

|

||||||||||||||||||

|

Comprehensive

income attributable to Mueller Industries, Inc.

|

$

|

16,684

|

$

|

893

|

$

|

134,780

|

||||||||||||||||||

|

See

accompanying notes to consolidated financial statements.

|

||||||||||||||||||||||||

|

(In

thousands)

|

2009

|

2008

|

||||||

|

Raw

materials and supplies

|

$

|

32,593

|

$

|

57,536

|

||||

|

Work-in-process

|

37,923

|

39,018

|

||||||

|

Finished

goods

|

126,184

|

122,756

|

||||||

|

Valuation

reserves

|

(5,438

|

)

|

(8,701

|

)

|

||||

|

Inventories

|

$

|

191,262

|

$

|

210,609

|

||||

|

(In

thousands)

|

2009

|

2008

|

||||||

|

Land

and land improvements

|

$

|

12,492

|

$

|

12,569

|

||||

|

Buildings

|

112,677

|

110,541

|

||||||

|

Machinery

and equipment

|

577,595

|

563,984

|

||||||

|

Construction

in progress

|

2,643

|

4,678

|

||||||

|

705,407

|

691,772

|

|||||||

|

Less

accumulated depreciation

|

(455,012

|

)

|

(414,845

|

)

|

||||

|

Property,

plant, and equipment, net

|

$

|

250,395

|

$

|

276,927

|

||||

|

(In

thousands)

|

Plumbing

& Refrigeration Segment

|

OEM

Segment

|

Total

|

|||||||||

|

Balance

at December 29, 2007:

|

||||||||||||

|

Goodwill

|

$

|

146,048

|

$

|

9,971

|

$

|

156,019

|

||||||

|

Accumulated

impairment

|

(2,756

|

)

|

—

|

(2,756

|

)

|

|||||||

|

143,292

|

9,971

|

153,263

|

||||||||||

|

Foreign

currency translation adjustment

|

(6,077

|

)

|

—

|

(6,077

|

)

|

|||||||

|

Impairment

charge

|

(18,000

|

)

|

—

|

(18,000

|

)

|

|||||||

|

Balance

at December 27, 2008:

|

||||||||||||

|

Goodwill

|

139,971

|

9,971

|

149,942

|

|||||||||

|

Accumulated

impairment

|

(20,756

|

)

|

—

|

(20,756

|

)

|

|||||||

|

119,215

|

9,971

|

129,186

|

||||||||||

|

Foreign

currency translation adjustment

|

1,713

|

—

|

1,713

|

|||||||||

|

Impairment

charge

|

(18,678

|

)

|

(9,971

|

)

|

(28,649

|

)

|

||||||

|

Balance

at December 26, 2009:

|

||||||||||||

|

Goodwill

|

141,684

|

9,971

|

151,655

|

|||||||||

|

Accumulated

impairment

|

(39,434

|

)

|

(9,971

|

)

|

(49,405

|

)

|

||||||

|

$

|

102,250

|

$

|

—

|

$

|

102,250

|

|||||||

|

(In

thousands)

|

2009

|

2008

|

||||||

|

6%

Subordinated Debentures, due 2014

|

$

|

148,176

|

$

|

148,676

|

||||

|

2001

Series IRB’s with interest at 3.08%, due 2011 through 2021

|

10,000

|

10,000

|

||||||

|

Mueller-Xingrong

line of credit with interest at 3.96%, due 2010

|

24,325

|

24,184

|

||||||

|

Other

|

50

|

50

|

||||||

|

182,551

|

182,910

|

|||||||

|

Less

current portion of debt

|

(24,325

|

)

|

(24,184

|

)

|

||||

|

Long-term

debt

|

$

|

158,226

|

$

|

158,726

|

||||

|

(In

thousands)

|

2009

|

2008

|

||||||

|

Cumulative

foreign currency translation adjustment

|

$

|

(8,503

|

)

|

$

|

(21,781

|

)

|

||

|

Unrecognized

prior service cost, net of income tax

|

(214

|

)

|

(408

|

)

|

||||

|

Unrecognized

actuarial net loss, net of income tax

|

(27,686

|

)

|

(22,101

|

)

|

||||

|

Unrecognized

derivative gains (losses), net of income tax

|

190

|

(3,907

|

)

|

|||||

|

Unrealized

gain on marketable securities, net of income tax

|

109

|

84

|

||||||

|

Accumulated

other comprehensive loss

|

$

|

(36,104

|

)

|

$

|

(48,113

|

)

|

||

|

(In

thousands)

|

2009

|

2008

|

2007

|

|||||||||

|

Domestic

|

$

|

36,478

|

$

|

131,472

|

$

|

168,936

|

||||||

|

Foreign

|

(13,349

|

)

|

(10,530

|

)

|

14,927

|

|||||||

|

Income

before income taxes

|

$

|

23,129

|

$

|

120,942

|

$

|

183,863

|

||||||

|

(In

thousands)

|

2009

|

2008

|

2007

|

|||||||||

|

Current

tax expense (benefit):

|

||||||||||||

|

Federal

|

$

|

14,834

|

$

|

40,743

|

$

|

62,215

|

||||||

|

Foreign

|

3,248

|

3,356

|

3,735

|

|||||||||

|

State

and local

|

2,264

|

(1,302

|

)

|

(1,238

|

)

|

|||||||

|

Current

tax expense

|

20,346

|

42,797

|

64,712

|

|||||||||

|

Deferred

tax (benefit) expense:

|

||||||||||||

|

Federal

|

(4,321

|

)

|

(3,686

|

)

|

2,379

|

|||||||

|

Foreign

|

3,893

|

(3,204

|

)

|

7,061

|

||||||||

|

State

and local

|

(2,126

|

)

|

2,425

|

(6,346

|

)

|

|||||||

|

Deferred

tax (benefit) expense

|

(2,554

|

)

|

(4,465

|

)

|

3,094

|

|||||||

|

Income

tax expense

|

$

|

17,792

|

$

|

38,332

|

$

|

67,806

|

||||||

|

(In

thousands)

|

2009

|

2008

|

2007

|

|||||||||

|

Expected

income tax expense

|

$

|

8,095

|

$

|

41,701

|

$

|

64,148

|

||||||

|

State

and local income tax, net of federal benefit

|

2,844

|

3,920

|

6,497

|

|||||||||

|

Effect

of foreign statutory rate different from U.S. and other foreign

adjustments

|

435

|

(1,015

|

)

|

603

|

||||||||

|

Valuation

allowance changes

|

52

|

(246

|

)

|

(1,920

|

)

|

|||||||

|

Adjustment

for the correction of prior year tax provision

|

—

|

—

|

2,239

|

|||||||||

|

U.S.

production activities deduction

|

(700

|

)

|

(2,275

|

)

|

(3,150

|

)

|

||||||

|

Gain

on early retirement of debt

|

(45

|

)

|

(7,551

|

)

|

—

|

|||||||

|

Goodwill

impairment

|

8,728

|

6,321

|

966

|

|||||||||

|

Tax

contingency changes

|

(973

|

)

|

(1,740

|

)

|

(1,449

|

)

|

||||||

|

Other,

net

|

(644

|

)

|

(783

|

)

|

(128

|

)

|

||||||

|

Income

tax expense

|

$

|

17,792

|

$

|

38,332

|

$

|

67,806

|

||||||

|

(In

thousands)

|

2009

|

2008

|

||||||

|

Beginning

balance

|

$

|

9,546

|

$

|

12,232

|

||||

|

Increases

related to prior year tax positions

|

4,824

|

1,356

|

||||||

|

Increases

related to current year tax positions

|

842

|

77

|

||||||

|

Decreases

related to prior year tax positions

|

(420

|

)

|

(2,677

|

)

|

||||

|

Decreases

related to settlements with taxing authorities

|

(226

|

)

|

(476

|

)

|

||||

|

Decreases

due to lapses in the statute of limitations

|

(3,284

|

)

|

(966

|

)

|

||||

|

Ending

balance

|

$

|

11,282

|

$

|

9,546

|

||||

|

(In

thousands)

|

2009

|

2008

|

||||||

|

Deferred

tax assets:

|

||||||||

|

Accounts

receivable

|

$

|

2,165

|

$

|

2,622

|

||||

|

Inventories

|

5,283

|

5,290

|

||||||

|

OPEB

and accrued items

|

14,126

|

14,816

|

||||||

|

Pension

|

13,753

|

13,438

|

||||||

|

Other

reserves

|

13,670

|

13,364

|

||||||

|

Interest

|

—

|

2,272

|

||||||

|

Federal

and foreign tax attributes

|

9,010

|

11,030

|

||||||

|

State

tax attributes, net of federal benefit

|

32,864

|

32,956

|

||||||

|

Other

|

2,105

|

1,902

|

||||||

|

Total

deferred tax assets

|

92,976

|

97,690

|

||||||

|

Less

valuation allowance

|

(33,812

|

)

|

(32,624

|

)

|

||||

|

Deferred

tax assets, net of valuation allowance

|

59,164

|

65,066

|

||||||

|

Deferred

tax liabilities:

|

||||||||

|

Property,

plant, and equipment

|

52,139

|

58,617

|

||||||

|

Foreign

withholding tax

|

606

|

1,652

|

||||||

|

Pension

|

8,357

|

7,855

|

||||||

|

Other

|

720

|

1,276

|

||||||

|

Total

deferred tax liabilities

|

61,822

|

69,400

|

||||||

|

Net

deferred tax liability

|

$

|

2,658

|

$

|

4,334

|

||||

|

(In

thousands)

|

Pension

Benefits

|

Other

Benefits

|

||||||||||||||

|

2009

|

2008

|

2009

|

2008

|

|||||||||||||

|

Change

in benefit obligation:

|

||||||||||||||||

|

Obligation

at beginning of year

|

$

|

146,505

|

$

|

180,231

|

$

|

21,969

|

$

|

19,438

|

||||||||

|

Service cost

|

865

|

1,783

|

235

|

310

|

||||||||||||

|

Interest

cost

|

8,907

|

11,472

|

1,824

|

1,379

|

||||||||||||

|

Participant

contributions

|

73

|

454

|

—

|

—

|

||||||||||||

|

Actuarial

loss (gain)

|

15,745

|

(19,254

|

)

|

(1,492

|

)

|

2,314

|

||||||||||

|

Benefit

payments

|

(12,281

|

)

|

(10,119

|

)

|

(1,152

|

)

|

(1,348

|

)

|

||||||||

|

Effect

of curtailments and settlements

|

—

|

—

|

(54

|

)

|

103

|

|||||||||||

|

Foreign

currency translation adjustment

|

4,830

|

(18,062

|

)

|

51

|

(227

|

)

|

||||||||||

|

Obligation

at end of year

|

164,644

|

146,505

|

21,381

|

21,969

|

||||||||||||

|

Change

in fair value of plan assets:

|

||||||||||||||||

|

Fair

value of plan assets at beginning of year

|

135,624

|

199,062

|

—

|

—

|

||||||||||||

|

Actual

return on plan assets

|

17,634

|

(42,933

|

)

|

—

|

—

|

|||||||||||

|

Employer contributions

|

3,244

|

2,387

|

1,152

|

1,348

|

||||||||||||

|

Participant contributions

|

73

|

454

|

—

|

—

|

||||||||||||

|

Benefit payments

|

(12,281

|

)

|

(10,119

|

)

|

(1,152

|

)

|

(1,348

|

)

|

||||||||

|

Foreign currency translation adjustment

|

3,409

|

(13,227

|

)

|

—

|

—

|

|||||||||||

|

Fair

value of plan assets at end of year

|

147,703

|

135,624

|

—

|

—

|

||||||||||||

|

Underfunded

status at end of year

|

$

|

(16,941

|

)

|

$

|

(10,881

|

)

|

$

|

(21,381

|

)

|

$

|

(21,969

|

)

|

||||

|

(In

thousands)

|

Pension

Benefits

|

Other

Benefits

|

||||||||||||||

|

2009

|

2008

|

2009

|

2008

|

|||||||||||||

|

Unrecognized

net actuarial loss

|

$

|

38,565

|

$

|

29,265

|

$

|

2,472

|

$

|

4,117

|

||||||||

|

Unrecognized

prior service cost

|

298

|

604

|

42

|

44

|

||||||||||||

|

(In

thousands)

|

Pension

Benefits

|

Other

Benefits

|

||||||||||||||

|

2009

|

2008

|

2009

|

2008

|

|||||||||||||

|

Long-term

asset

|

$

|

3,772

|

$

|

2,820

|

$

|

—

|

$

|

—

|

||||||||

|

Current

liability

|

—

|

—

|

(1,423

|

)

|

(1,452

|

)

|

||||||||||

|

Long-term

liability

|

(20,713

|

)

|

(13,701

|

)

|

(19,958

|

)

|

(20,517

|

)

|

||||||||

|

Total

underfunded status

|

$

|

(16,941

|

)

|

$

|

(10,881

|

)

|

$

|

(21,381

|

)

|

$

|

(21,969

|

)

|

||||

|

(In

thousands)

|

2009

|

2008

|

2007

|

|||||||||

|

Pension

benefits:

|

||||||||||||

|

Service

cost

|

$

|

865

|

$

|

1,783

|

$

|

2,410

|

||||||

|

Interest

cost

|

8,907

|